One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into hearts. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

Decline in Audit Rates

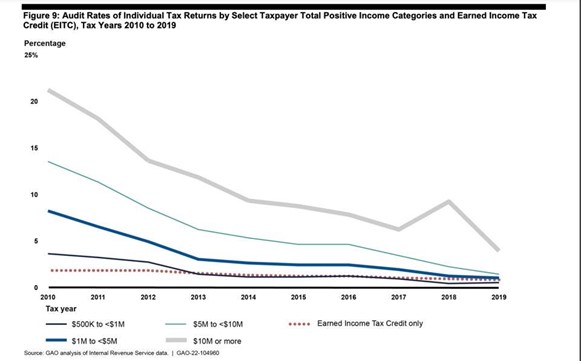

The rate at which the IRS is auditing individual taxpayers has declined overall between the years 2010 and 2019 (2020 data is too new and 2021 returns are still being filed through the extension period). According to the Government Accountability Office (GAO), nearly 1 percent of all taxpayers were audited in 2010, compared to only 0.25 percent for the tax year 2019. The GAO chart below shows the ski slope-like drop in individual tax audit rates over the period.

While the IRS continues to audit higher-earning taxpayers more often overall, during the 10 years charted, audit rates consistently declined for all levels of taxpayers, except those with the highest incomes. The audit rate for taxpayers with income between $200k and $500k experienced the largest drop, with the audit rate declining from 2.3 percent down to 0.2 percent; a 92 percent reduction in audits. Taxpayers with the highest incomes, defined as $10 million or more, saw a resurgence in audit rates from 2017-2018; however, even they experienced an overall decline, dropping from 21.2 percent in 2019 to only 3.9 percent in 2019 – equating to an 81 percent decline.

Impact on the Treasury

There is a theory that the prospect of a tax audit leads to greater voluntary compliance. In other words, if people think they won’t get audited, then they are more likely to cheat on their taxes.

Non-compliance with tax laws and regulations has a material impact on the Treasury. According to the IRS, it is estimated that on average, individual taxpayers under-reported nearly $250 billion a year for the period 2011-2013. This leads to the non-collection of taxes that are otherwise owed to the government and raises issues of fairness for taxpayers who are playing by the rules.

Why the Decline in Audit Rates?

One of the main drivers is a lack of resources at the IRS, a combination of both reduced funding and fewer auditors on staff. The number of agents working for the IRS has declined across the board since 2011. Tax examiners, the type who handle basic audits by mail, have dropped by 18 percent. Meanwhile, revenue agents, who handle the more complex cases in the field, declined by more than 40 percent over the same period.

Demographics point to an increase in these trends as there is a wave of coming retirements in the IRS. Over the next three years, nearly 14 percent of current tax examiners and 16 percent of revenue agents are expected to retire. Stack on top of this is the fact that the inexperience of newer agents and the time to complete audits is also taking longer.

Conclusion

The IRS claims it is missing out on millions in legally due tax revenues due to the inability to maintain enforcement. They say they need more funding to hire more agents to perform more audits, which not only find fraud in the audits themselves but also increase overall compliance due to the pressure this creates.

Currently, there is no political focus on bringing significant new resources to the IRS, so we are not likely to see an uptick in individual tax audit rates anytime soon. The trend of focusing on the highest earners, however, will likely continue as this is where the IRS can find the most bang for its buck.