Categories for

How to Clean Up QuickBooks for 2020

Yes, it’s here again: the end of the year. You probably have a lengthy to-do list full of tasks that must be done before December 31. There’s one task—or rather, a series of tasks—that you should definitely add to that list: year-end QuickBooks cleanup. Following the guidelines provided here will do three things. It will:

- Ensure that you’ve processed every 2019 transaction (or that you know why you can’t).

- Give you a sense of closure, knowing that you’ve dealt with all your 2019 financial data.

- Allow you to start your 2020 QuickBooks activities with as clean of a slate as possible.

First Things First

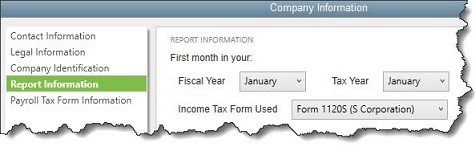

Before you start looking at transactions and running reports, check to make sure that your fiscal year is recorded correctly in QuickBooks. Open the Company menu and select My Company. Click the pencil icon in the upper right to open the Company Information window, then click Report Information in the tabs to the left. This window opens:

Is your company’s fiscal year recorded correctly in QuickBooks? If not, please contact us. Don’t try to fix this on your own.

Account For All Of Your Income

You certainly want to have received all the money owed to you by December 31 if at all possible. So, run a report to see which customers have outstanding, overdue balances. Open the Reports menu and select Customers & Receivables | A/R Aging Summary.

The first column here will read Current. You don’t have to worry about these customers. It’s the next four columns that will require follow-up. If your default payment terms are 30 days, you’ll see columns for 1-30, 31-60, 61-90, and >90. Customers with dollar amounts in those columns have not met their obligations and are past due by those date ranges.

Note: If your default terms are different (like 15 days), you’ll need to customize the report. In the toolbar at the top, you’ll see a field labeled Interval (days). Change it to reflect your own default terms and click Refresh in the upper right corner.

If your report contains only a sea of zeroes in those four columns, everyone is paid up. If not, you can send statements to anyone who is at least one day past due to remind them of what they owe. Open the Customers menu and select Create Statements to see this window:

Partial view of the Create Statements window

Make sure the Statement Date is correct since QuickBooks will use this to calculate aging. Then you can either enter a specific Statement Period or request All open transactions as of Statement Date. If you choose the latter, you’ll most likely want to limit the statements to customers whose payments are overdue. So, you’d click in the box in front of Include only transactions over [your number here] days past due date.

Below these options, you’ll be able to indicate which customers should receive statements. The most common choice is All Customers (who fall into the group you just defined), but you can also send to one or multiple customers, for example. QuickBooks will display a list if you select one of these. The right pane of this window contains several additional options that you can check or uncheck. When you’re satisfied, you can Preview, Print, or E-mail the statements.

Pay Outstanding Bills

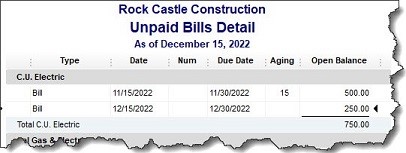

You should also try to settle your Accounts Payable before the end of the year. Open the Reports menu and select Vendors & Payables | A/P Aging Summary. Look for dollar amounts in the columns that show aging beyond the first column. You can also run the Unpaid Bills Detail report and look at the Aging column, as pictured here:

Look in the aging column of this report to see which bills are past due and by how many days.

Note: QuickBooks has multiple Preferences that relate to reports and aging. We can go over these with you if you haven’t explored them.

There are other tasks you should complete before December 31, some of which may require our assistance. These include reconciling all accounts, running year-end reports, and clearing any deposits that remain in the Undeposited Funds account. We’re here if you need us now, otherwise we can connect in the New Year.

Year-End Tips for Charitable Contributions

As the end of the year and the holiday season approach, we will all see an uptick in the number of charitable solicitations arriving in our mailboxes and by email. Since some charities sell their contributor lists to other charities, frequent contributors may find themselves besieged by requests from all sorts of charities with which they are not familiar.

Watch Out for Charity Scams – You need to be careful, as scammers out there are pretending to be legitimate charities looking to take advantage of your generosity for their gain.

When making a donation to a charity with which you are unfamiliar, you should take a few extra minutes to ensure that your gifts are going to legitimate charities. The IRS has a search feature, Tax Exempt Organization Search, which allows people to find legitimate, qualified charities to which donations may be tax-deductible. You can always deduct gifts to churches, synagogues, temples, mosques, and government agencies—even if the Tax Exempt Organization Search tool does not list them in its database.

Here are some tips to make sure your contributions go to legitimate charities.

- Be wary of charities with names that are similar to familiar or nationally known organizations. Some phony charities use names or websites that sound or look like those of respected, legitimate organizations.

- Don’t give out personal financial information, such as Social Security numbers or passwords, to anyone who solicits a contribution from you. Scam artists may use this information to steal your identity and money. Using a credit card to make legitimate donations is quite common, but please be very careful when you are speaking with someone who calls you; don’t give out your credit card number unless you are certain the caller represents a legitimate charity.

- Don’t give or send cash. For security and tax-record purposes, contribute by check, credit card, or another way that provides documentation of the gift.

Another long-standing type of abuse or fraud involves scams that occur in the wake of significant natural disasters. In the aftermath of major disasters, it’s common for scam artists to impersonate charities to get money or private information from well-intentioned taxpayers. Scam artists can use a variety of tactics. Some scammers operating bogus charities may contact people by telephone or email to solicit money or financial information, and they may set up phony websites claiming to solicit funds on behalf of disaster victims. Unscrupulous individuals may even directly contact disaster victims and claim to be working for or on behalf of the IRS to help the victims file casualty loss claims to get tax refunds.

Scammers may also attempt to get personal financial information or Social Security numbers, which can be used to steal the victims’ identities or financial resources. Disaster victims with specific questions about tax relief or disaster-related tax issues can visit the IRS website for Disaster Assistance and Emergency Relief for Individuals and Businesses.

Tax Benefits of Charitable Contributions – Contributions to charitable organizations are deductible if you itemize your deductions on Schedule A. Generally, the deduction is the lesser of your total contributions for the year or 50% of your adjusted gross income, but the 50% is increased to 60% for cash contributions in years 2018 through 2025, and lower percentages may apply for non-cash contributions and certain types of organizations. Itemized deductions reduce your gross income when determining your taxable income.

However, with the increase in the standard deduction as a result of the 2017 tax reform, many taxpayers are no longer itemizing their tax deductions (because the standard deduction provides a greater tax benefit). For those in this situation, there are two possible workarounds:

- Bunching Deductions – The tax code allows most taxpayers to utilize the standard deduction or itemize their deductions if doing so provides a greater benefit. As a rule, most taxpayers just wait until tax time to add everything up and then use the higher of the standard deduction or their itemized deductions. If you want to be more proactive, you can time the payments of tax-deductible items to maximize your itemized deductions in one year and take the standard deduction in the next.

- Qualified Charitable Distributions – Individuals age 70½ or older – who must withdraw annual required minimum distributions (RMDs) from their IRAs—are allowed to annually transfer up to $100,000 from their IRAs to qualified charities. Here is how this provision works, if utilized:

(1) The IRA distribution is excluded from income;

(2) The distribution counts toward the taxpayer’s RMD for the year; and

(3) The distribution does NOT count as a charitable contribution deduction.

At first glance, this may not appear to provide a tax benefit. However, by excluding the distribution, a taxpayer lowers his or her adjusted gross income (AGI), which helps with other tax breaks (or punishments) that are pegged at AGI levels, such as medical expenses when itemizing deductions, passive losses, and taxable Social Security income. In addition, non-itemizers essentially receive the benefit of a charitable contribution to offset the IRA distribution.

Substantiation – Charitable contributions are not deductible if you cannot substantiate them. Forms of substantiation include a bank record (such as a cancelled check) or a written communication from the charity (such as a receipt or a letter) showing the charity’s name, the date of the contribution, and the amount of the contribution. In addition, if the contribution is worth $250 or more, the donor must also get an acknowledgment from the charity for each deductible donation.

Non-cash contributions are also deductible. Generally, contributions of this type must be in good condition, and they can include food, art, jewelry, clothing, furniture, furnishings, electronics, appliances, and linens. Items of minimal value (such as underwear and socks) are generally not deductible. The deductible amount is the fair market value of the items at the time of the donation; as with cash donations, if the value is $250 or more, you must have an acknowledgment from the charity for each deductible donation. Be aware: the door hangers left by many charities after picking up a donation do not meet the acknowledgement criteria; in one court case, taxpayers were denied their charitable deduction because their acknowledgement consisted only of door hangers. When a non-cash contribution is worth $500 or more, the IRS requires Form 8283 to be included with the return, and when the donation is worth $5,000 or more, a certified appraisal is generally required.

Special rules also apply to donations of used vehicles when the claimed deduction exceeds $500. The deductible amount is based upon the charity’s use of the vehicle, and Form 8283 is required. A charity accepting used vehicles as donations must provide Form 1098-C (or an equivalent) to properly document the donation.

Don’t be scammed; make sure you are donating to recognized charities. Donations to charities that are not legitimate are not tax-deductible. Contributions to legitimate charities need to be properly substantiated if you plan to claim them as part of your itemized deductions. If you have any questions related to charitable giving, please give our office a call.

Tax Changes For 2019

As the end of the year approaches, now is a good time to review the various changes that impact 2019 tax returns. Some of the changes are likely to apply to your tax situation. In addition, be aware that various tax-related bills currently in Congress may or may not pass this year. If any of them do pass, we will quickly get the details to you.

Medical Threshold – Medical expenses are deductible as itemized deductions only if the total medical expenses for the tax year exceed a specified percentage of a taxpayer’s income. After dropping to 7.5% for 2017 and 2018, this threshold reverts to 10% for 2019. As a result, any medical expenses from 2019 are deductible only to the extent that they exceed 10% of a taxpayer’s adjusted gross income for the year.

Electric Vehicle Credit Phaseout – As an incentive to get taxpayers to move away from conventional-fuel (gasoline or diesel) vehicles, Congress has provided tax credits of up to $7,500 for the purchase of plug-in electric vehicles. However, Congress’s rules limit the full credit to the first 200,000 vehicles sold by a given manufacturer. Once a company sells 200,000 qualifying vehicles, the credit begins to phase out for that company. Tesla, Chevrolet, and Cadillac have all reached the phaseout point. The table below shows the credits available depending upon the quarter when the vehicle is purchased.

| Vehicles Beginning Phaseout out 2019 | |||||||

| Date Acquired >>> Vehicle |

Before 2019 | Jan – Mar 2019 | Apr – June 2019 | July – Sept 2019 | Oct – Dec 2019 | Jan – Mar 2020 | After Mar 2020 |

| Tesla* | $7,500 | $3,750 | $3,750 | $1,875 | $1,875 | $0 | $0 |

| Chevrolet* | $7,500 | $7,500 | $3,750 | $3,750 | $1,875 | $1,875 | $0 |

| Cadillac* | $7,500 | $7,500 | $3,750 | $3,750 | $1,875 | $1,875 | $0 |

*All qualifying models

If a qualifying vehicle is used partiality for business, the credit is proportionally allocated between personal and business tax credits. The personal portion can only offset the individual’s current-year tax liability; any excess is lost. The business portion can be carried back for one year and then forward up to 20 years until it is used up; any credit remaining after the 20th year is lost. As a tip, please note that the credit limit is per vehicle, not per taxpayer, so individuals who make multiple purchases can receive multiple credits.

Alimony – One delayed effect of the 2017 tax reform is that, the treatment of alimony changes for some individuals starting in 2019.

For divorces or separations entered into before 2019, alimony payments continue to be deductible for the payer and taxable for the recipient; such payments also still qualify as earned income for purposes of the recipient’s qualification for an IRA deduction. For divorces or separations executed after December 31, 2018, alimony payments are no longer deductible for the payer. In addition, for the recipient, they are no longer taxable income and do not count as earned income for the purposes of IRA deduction.

Divorces or separations entered into before 2019 continue to follow the pre-2019 rules unless they have been modified after December 31, 2018; in that case, the alimony payments are subject to the post-2018 rules if the modification expressly provides for this.

Finalization of State- and Local-Tax Deduction Limitation – The 2017 tax reform limited the itemized deduction for state and local taxes (SALT) to $10,000 (or $5,000 for married individuals filing separately). This has adversely impacted taxpayers in high-tax states such as California, Connecticut, New Jersey, and New York. Elected officials in several states have attempted to work around this restriction by establishing (or proposing to establish) state charities. The idea is that taxpayers would make deductible contributions that, in return, would give them tax credits against their SALT equal to most of the value of the charitable contributions. Unfortunately, these officials have overlooked the 1986 U.S. Supreme Court ruling that, if a taxpayer receives something in return for a contribution (i.e., a quid pro quo), the contribution is not deductible.

The final regulations generally reduce the charitable-contribution deduction by the amount of any SALT credit received. However, as an exception, if the credit does not exceed 15% of the contribution, the entire contribution is deductible.

Penalty for Not Being Insured – The Tax Cuts and Jobs Act (tax-reform) that was enacted at the end of 2017 eliminated the Obamacare shared-responsibility payment, effective starting in 2019. Congress didn’t actually repeal this penalty; instead, it effectively repealed it by tweaking by setting zero values for both the percentage of household income used in the calculation and the flat dollar amount of the penalty. As a result, the amount of the penalty is always zero. However, keep in mind that the penalty could be restored in the future if the direction that the political winds are blowing changes. In addition, beginning in 2020, some states may pick up where the federal government left off and charge a penalty to residents without qualified health insurance coverage.

Qualified Opportunity Funds – Taxpayers who receive capital gains on the sale or exchange of property (if the other party is unrelated) may elect to defer – and, potentially, partially exclude – those gains from their gross income if they are reinvested in a qualified opportunity fund (QOF) within 180 days of the sale or exchange. The amount of the gain (not the amount of the proceeds, as in Sec. 1031 deferrals) needs to be reinvested in order to defer the gain. The deferral period ends when the QOF investment ends or on December 31, 2026 – whichever is sooner. At that time, taxes must be paid on the deferred gain.

However, 10% of the deferred gains are forgiven QOF investments have been held for at least 5 years, and 15% of the gains are forgiven when those investments have been held for at least 7 years. Note that, with the deferral end date of December 31, 2026, qualifying for the 15% forgiveness requires a QOF investment on or before December 31, 2019.

Seniors Get a Special Tax Form – Lawmakers have long sought to provide taxpayers who are age 65 and older with a simplified tax form in place of the Form 1040. In the 2018 budget bill, Congress finally included a requirement that the IRS create such a form. As a result, the IRS will introduce Form 1040-SR, which will look a lot like the old form looked before the 2018 tax reform instituted its (politically motivated) division of the Form 1040 into multiple postcard-size schedules. It is unclear how much simpler the Form 1040-SR will be, but it will be available for 2019 returns. Form 1040-SR will be optional.

Family and Medical Leave Credit – The employer credit for family and medical leave, which was created in the 2017 tax reform, ends after 2019. This two-year program provides employers with a tax credit equal to 12.5% of the wages they paid to qualifying employees during any period when those employees were on family and medical leave, provided that the rate of the leave payments are at least 50% of the employees’ normal wages. The credit can be claimed for a maximum of 12 weeks of leave for any employee during the tax year. For each percentage point for which the leave payments exceed 50% of normal wages, this credit increases by 0.25 percentage points (up to a maximum of 25%). Participation in this credit program is optional.

Inflation Adjustments – Just about every tax-related value is adjusted for inflation. Some values are adjusted for any level of change, but others are adjusted only if the change reaches at least a specific dollar amount (so these values may not change every year). The table below includes the actual 2019 inflation adjustments and the projected 2020 adjustments for some of the most frequently encountered values.

| Year | 2018 | 2019 | 2020 |

| Standard Deduction | |||

| Single or Married Filing Separately | 12,000 | 12,200 | 12,400 |

| Head of Household | 18,000 | 18,350 | 18,650 |

| Married Filing Jointly | 24,000 | 24,400 | 24,800 |

| Additional Standard Deduction (Age 65+ or Blind) | |||

| Unmarried | 1,600 | 1,650 | 1,650 |

| Married | 1,300 | 1,300 | 1,300 |

| Other Values | |||

| Annual Gift-Tax Exclusion | 15,000 | 15,000 | 15,000 |

| Foreign Earned-Income Exclusion | 103,900 | 105,900 | 107,600 |

| IRA Contribution Limit | 5,500 | 6,000 | 6,000 |

| IRA Contribution Limit (Age 50+) | 6,500 | 7,000 | 7,000 |

| 401(k) Contribution Limit | 18,500 | 19,000 | * |

| 401(k) Contribution Limit (Age 50+) | 24,500 | 25,000 | * |

All values are in U.S. dollars.

* Value not available as of publication

Form W-4 Revision – During the previous tax season, many people received a smaller federal tax refund than normal or actually owed taxes despite usually getting a refund. In most cases, this was due to the last-minute passage of the tax-reform law at the end of 2017, which did not give the IRS not sufficient time to adjust the W-4 form and related computation tables for the 2018 tax year so as to account for all of the new law’s changes. The planned major revision to the W-4 for the 2019 tax year has since been delayed until 2020, so all taxpayers should make sure that their 2019 withholding is adequate.

If you are conversant with tax terminology, you can use the IRS’s newly updated withholding estimator. This tool helps taxpayers to determine whether their employers are withholding the right amount of tax from their paychecks. However, please note that the results are only as good as the information that is put into the estimator. Users need to properly estimate their other income for the year from various sources.

If you have questions related to any of the subjects discussed in this article, be sure to give our office a call.

Gross Domestic Product: A Primer

The economic indicator known as Gross Domestic Product (GDP) represents the dollar value of all purchased goods and services over the course of one year. It is comprised of purchases from all private and public consumption, including for-profit, nonprofit and government sectors.

There are four components that are added to calculate the GDP:

- Consumer spending

- Government spending

- Investment spending (this includes business, inventory, residential construction and public investment)

- Net exports (the value of goods exported minus the value of goods imported)

The government calculates and publishes the GDP rate on a quarterly basis and for the entire year.

What Affects GDP?

There are different ways GDP is measured, nominal and real. Nominal GDP refers to a straight calculation of raw data, while real GDP adjusts the calculation to include the impact of inflation.

When inflation increases, real GDP tends to rise; when prices drop, so does real GDP. Be aware that this adjustment can happen even when there is no change in the quantity of goods and services produced in the United States during that time frame.

A key component of the GDP calculation is net exports. This number rises when the country sells more goods and services to foreign countries than it buys from them. A trade surplus means the United States sells more than it purchases, which is a strong contributor to GDP. When the United States buys more foreign goods than it sells, this creates a trade deficit, which is a negative weight in the GDP calculation.

GDP also reflects demand. The dollar output of certain sectors and industries rises and falls based on the popularity of their products and services. For example, when a new product is well received, then those sales increase that sector’s contribution to GDP. This is a helpful measure because it enables companies to make better research and development decisions based on recent success. The same is true when a new product, or even an upgrade to a new product, does not increase sales.

What Does GDP Indicate?

GDP is the most common, broad-based measure used to monitor the country’s economic progress. When it is on the rise, the economy is considered to be growing. When GDP drops – even if it remains in positive territory – the economy is viewed as contracting. If GDP continues to slip quarter after quarter, this is an indicator that the economy might be in trouble and the Federal Reserve or Congress could consider altering monetary (interest rates) or fiscal (taxes and government spending) policy to inject cash into the nation’s financial system.

Technically, economists define a recession as a prolonged period of economic decline, often precipitated by two consecutive quarters of negative GDP growth.

This economic yardstick also is used to indicate a country’s general standard of living. The better a country is able to produce the goods and services that its residents and businesses use, the more that capital is infused back into the country. Therefore, higher GDP levels indicate a more prosperous country and relatively higher standard of living among its residents.

GDP doesn’t just gauge domestic economic health; it serves as a comparison measure to other countries. This is particularly important during periods of growth and decline because the United States can track how well it is responding to global economic factors relative to other countries.

Current Trendline

According to the Bureau of Economic Analysis, first quarter real GDP closed at 3.1 percent. In the second quarter, real GDP fell to 2.0 percent. The advanced assessment for the third quarter of 2019 is 1.9 percent.

Employee Spotlight – Jessica Peiffer

Jessica Peiffer joined Ross Buehler Falk (RBF) in 2019, establishing herself in the accounting industry. In her capacity as an accountant, she works primarily in the firm’s Audit Department. Jessica sits on the RBF Fun Committee, where she helps generate ideas for fun and exciting things the office can do as a team.

Since she is relatively new to the accounting field, Jessica has yet to establish an area of specialty. “I do, however, feel my strengths would pertain to any area of construction and real estate, due to my extensive background in these related fields,” she explained. Jessica is referring to the four and a half years she spent working in property management and real estate and the 11 years she devoted to home improvement. Prior to joining RBF she developed extensive experience in management, sales, assistance with the purchase of properties, and home renovations.

When asked to describe her personal philosophy of service, Jessica replied, “I want to treat each client and customer like they are the only thing that matters and make it clear that I see them as a person, not a number.” Jessica chose to go into accounting because she has always been intrigued with the logic of numbers. She likes that they work in a way that is “matter of fact” and leaves no room for gray area. This, in combination with her naturally investigative mind, makes her a great fit for the field.

Jessica’s favorite quote comes from Albert Einstein: “Creativity is intelligence having fun.” She loves it because she believes that if, as adults, we could maintain the creativity and imaginations we once had as children, the world would be a happier place. Jessica expresses this desire in her favorite hobby: painting. “I am a self-made artist who pushes the boundaries of color exploration,” she explained. Jessica’s portfolio of commissions includes tattoo designs/drawings and a variety of paintings ranging from abstract to feminine exploration. “This allows me to express who I am as an artist while catering to the wants of others. The feeling and satisfaction gained from providing a client with a piece of art that stirs their emotions and overwhelms them with happiness is simply one of the best.”

Raised in Lebanon, Pennsylvania, Jessica currently lives in Mount Joy. She enjoys the area because it offers a good mix of close by activities and greenery, farmland, animals, and nature. Jessica is mother to two beautiful girls and has a zoo of animals, including two dogs, a cat, a hamster, and some fish. She cites her mother and grandmother as the most influential people in her personal life, and Vincent Van Gogh as her biggest creative inspiration.

Payroll Management Tips

When it comes to an employer’s responsibility for non-exempt workers, according to the U.S. Department of Labor, there are many requirements businesses must follow related to payroll. In one example, there are strict regulations on what information employers must document for each non-exempt worker. While there’s no requirement on how the information is recorded, there are three main categories.

Personal details: This should include the employee’s name, complete address, Social Security number, date of birth and gender.

Job details: This must include the worker’s job description and hours clocked in each day and week.

Pay details: The employee’s hourly wage based on straight time, and how employees are compensated – be it hourly, weekly, by project or item-based. Records should include the number of hours worked each week, per day or per week non-overtime earnings, overtime earnings per work week, and the compensation paid to the employee for the pay period. Also included should be the day of the employee’s check, the time period of the work described, and all deductions or increases to the worker’s wages.

Depending on the type of record, employers have different time requirements for record archival. Payroll records must be maintained for 36 months. Schedules, timecards and deduction records for employee earnings must be held for 24 months and be readily accessible for inspection by the U.S. Department of Labor.

When there is minimal deviation from an employee’s schedule, employers simply have to confirm the employee adhered to the schedule. When there is a large deviation (working fewer or more hours than normally scheduled), the actual number of hours worked should be noted. It doesn’t matter how time is kept for an employee, as long as it’s kept – be it manually written by the worker, a supervisor or HR rep or with a time clock.

Other Documentation

The IRS explains that employers are required to complete Form W-2 to maintain compliance with tip and wage payments. This should be completed and submitted by the end of the calendar year.

Employees who fill out the Form W-4 can mitigate estimated tax liability by specifying how much to have withheld from their compensation by their employer. An employee can claim exemption from federal income tax withholding if she had no income tax liability the prior year and does not expect to pay taxes in the coming year. However, the employer is still required to deduct the FICA tax for that employee.

FICA Tax

Also known as the Federal Insurance Contributions Act (FICA), employers are required to withhold two different types of taxes: Social Security and Medicare. According to the Internal Revenue Service (IRS), employers are responsible to calculate and remit these taxes based upon each employee’s wages.

For the 2019 tax year, Social Security taxes for employer and employee are both 6.2 percent, or 12.4 percent total. This tax is limited to the first $132,900 in wages. The Medicare withholding rate is 1.45 percent of wages for both employer and employee, totaling 2.9 percent. Unlike Social Security taxes, for Medicare there’s no cap on the employee’s total salary. Additionally, for wages exceeding $200,000 for 2019, only the employee is taxed an additional 0.9 percent, in addition to the 1.45 percent (for a total of 2.35 percent of any wages exceeding $200,000 for the 2019 calendar tax year) for Medicare taxes.

Individual Estimated Taxes

Estimated Taxes are meant to satisfy many forms of taxes, and not just income tax obligations. They also includes the alternative minimum tax (AMT) and self-employment taxes. Whether it’s a single entrepreneur, a business partner or someone with equity in an S corporation, as long as they have $1,000 or greater in tax obligations, they have to pay estimated taxes, generally on a quarterly basis. When it comes to corporations, the threshold for estimated tax payments is $500 when they prepare their taxes. In addition to taxpayers under the tax liabilities outlined above, estimated taxes are not required for individuals who meet the following: there was no tax owed for the preceding year, the individual was a U.S. citizen or resident for the entire year, and the last tax year was for 12 months. Also note that self-employed workers must pay both the employer and employee portion of the FICA tax.

Much like the evolving landscaping of the U.S. Tax Code, the world of payroll is also subject to ongoing changes that are imperative to maintaining compliance.

Sources:

https://www.dol.gov/whd/regs/compliance/whdfs21.htm

https://www.irs.gov/businesses/small-businesses-self-employed/understanding-employment-taxes

How Will Tariff Developments Impact the Stock Market Going Forward?

According to an Aug. 13 press release from the office of the United States Trade Representative (USTR), there will be a 10 percent tariff levied against $300 billion of Chinese imports effective Sept. 1. The same press release announced a modification, after hearing from the public and business owners, exempting some of the $300 billion in Chinese imports from the 10 percent tariff until Dec. 15.

Items Subject to the 10 Percent Tariff on Sept. 1

Highlights from the USTR’s list include select types of coffee, fruit, vegetables, insects and bees. Along with dairy products, livestock such as sheep, horses and goats are subject to the 10 percent tariff.

Items Subject to the 10 Percent Tariff on Dec. 15

The USTR pointed out that many of the items recently exempted include consumer goods such as computer displays, select shoes and clothes, LED lamps, slide projectors and playing cards. Other items on the list include notebooks, video game systems, toys, snowshoes and parts, fishing rods and reels, paint rollers and microwave ovens.

2019 Forecast

When it comes to industry experts and associations, it looks like there will be limited impacts from the trade spat between the United States and China, coupled with pressure from government shutdown in the beginning of the year. According to the National Retail Federation (NRF), 2019 is expected to see an increase in spending between 3.8 percent and 4.4 percent – or more than $3.8 trillion.

Initial figures per the NRF detail that retail sales for 2018 increased by 4.6 percent, outpacing the organization’s growth expectations of 4.5 percent. 2018’s figures are compared to 2017’s of $3.68 trillion in retail sales. 2018’s estimates factor in a 10 percent to 12 percent increase in online sales, which is also expected for 2019. One caveat for these projections by the NRF is that it doesn’t include dining, gas stations or auto dealers. GDP is expected to grow about 2.5 percent over 2019.

The NRF explained that due to lower energy costs, specifically tame retail gas prices and low interest rates, there should be minimal negative consumer impact. However, the NRF cautions that while the retail industry has been able to cushion the 10 percent tariffs, if tariffs increase to 25 percent, there will be a greater impact on consumers’ costs and retailers’ profitability.

Based upon recent developments, business earnings will face greater challenges. According to the United States Trade Representative’s Aug. 23 press release, tariff rates for $250 billion worth of Chinese imports currently subject to a 25 percent tariff rate will increase to 30 percent effective Oct. 1. For the $300 billion in Chinese imports described above, those going into effect Sept. 1 and Dec. 15, instead of being subjected to a 10 percent tariff, each batch will be subject to a 15 percent tariff rate.

With the Congressional Budget Office (CBO) forecasting a drop in the United States’ gross domestic product (GDP) of 0.3 by 2020, Daniel Fried explains that there’s no doubt the U.S.-China trade tensions have and will take a toll on the economy. Fried explains how they’ll affect consumer spending and business expenditures:

- The initial impact is that consumers and businesses will have a lowered purchasing power.

- The next impact is that businesses will either slow or decide to divert investments elsewhere, such as realigning their supply chains to mitigate the tariff impacts.

- There’s also concern that while businesses may lose international business, that might be offset by domestic consumption.

With Fried and the CBO projecting the mean income for households will be reduced by $580 by 2020, based on 2019 purchasing power, it’ll certainly make consumers think twice about where and how to allocate their spending. This will likely take a toll on companies’ sales figures and likely future earnings reports.

The Checklist Every Small Business Owner Needs for New Hires

Growing your business to the point that you need to start hiring employees is exciting. It’s also rife with administrative burdens that you don’t want to be unprepared for.

When taking on a new hire, you need more than 1) the assurance your cash flow is sufficient to support your payroll expenses and 2) that the talent is the right fit for the role. There are governmental obligations to consider, as well as fitting your new employee into your existing schedule and structure. Small businesses face additional challenges when it comes to compliance, cash flow, and keeping operations on track. Follow this checklist to make the onboarding process run as smoothly as possible.

1. Get the new hire’s ID, work eligibility, and tax withholding forms in order before you do anything else.

Make a copy of the employee’s government-issued photo ID and confirm that the new hire is eligible to work in the United States. This requires filling out an I-9 form and checking with the government database that it’s valid. Neglecting to collect an I-9 at the time of onboarding can result in fines worth $375-$16,000 per violation, with another $100-$1,100 per violation if you fail to produce a valid I-9 for each employee at the time of inspection.

In order to make sure that the employee’s paychecks are calculated correctly from the first payroll period onward, you will need to collect a Form W-4. If your state and/or city has income taxes, you will also need state and local withholding forms. This is particularly important if your organization hires talent from multiple states, such as the greater New York City and Philadelphia areas. This is also the ideal time to get direct deposit forms filled out.

2. Order a background check.

Depending on the scope of the work performed, you may be held liable for your employees’ actions and deemed negligent in the hiring process if it turns out that they committed crimes in the past that are relevant to the job (such as larceny if hiring an inventory manager). Note: a nonviolent drug offense is less likely to have bearing on their lives nowadays. You may not need every piece of information that comes up in a background check or find it relevant to the position, but it can help ensure the safety and security of your clients, staff, and other stakeholders.

3. Enroll the employee in any benefit programs offered.

Even if there’s a grace period involved, it’s best to get a new hire onboarded into any benefit programs immediately so that neither of you has to be inconvenienced by manual enrollment in the future. Health insurance and retirement benefits are the most crucial benefits for immediate enrollment, but if you offer any other programs like pre-tax transit passes, flex accounts, and wellness plans (e.g. gym memberships), you also need to get the new hire enrolled or leave instructions on how to do so.

4. Walk the new hire through your business processes, policies and procedures.

Once all of the relevant government and payroll forms have been filled out and you’re ready to proceed, getting new employees familiar with the business environment and organizational culture is the next integral step of the onboarding process.

If you have an employee handbook, provide them with one. Outline the most critical policies that are most relevant to the job and maintaining an efficient and safe workplace such as code of conduct, dress code, guidelines for remote work and total hours worked, parking rules and other policies and procedures they need to be immediately aware of. If your workplace uses badges or employee IDs, arrange to have one made right away, and if necessary, get business cards with the employee’s name printed on them.

5. Arrange the new hire’s workspace.

Does your new hire have a desk and chair, a properly set up computer and any other tools that may be necessary? Or, if the position is not a desk job, do you have the required uniforms in the correct size, along with tools and any other occupational gear your new hire will need? Is the area properly furnished (if you recently expanded your workplace to make room for new hires)?

Other important aspects of readying the workspace that shouldn’t be overlooked include employee IDs (and updating any registries if located within a building or complex), keys, filing cabinets, employee e-mail addresses and intranet, and furnishing devices (if this is your policy).

6. Integrate new employees into the workplace.

Arrange for any meetings or lunches with the appropriate managers, clients, or key employees that new hires need to get to know better. Have them tour the workplace to get familiar with how it operates and make arrangements for training or additional resources that may be required. Make sure that the new hires also understand the required job duties and how they fit within the department or overall organization. Encourage questions and comments throughout the entire process.

Onboarding can be a stressful time for smaller organizations that are just starting to grow. But if you follow this checklist and get those critical forms out of the way first, transitioning a new hire can go smoothly.

5 Things You Should Know About the Chart of Accounts in QuickBooks Online

You probably didn’t expect you’d have to become an accounting expert when you started your business. You knew you’d have to deal with recording income and expenses – maybe track your inventory and process a payroll. But you may not have understood just how complex financial bookkeeping could be.

That’s why you decided to use QuickBooks Online, or are at least considering it. The service is an expert on accounting, and it simplifies the process. It knows exactly how you have to document transactions to stay compliant with the rules that accountants and other businesses follow. This is good practice, and it’s absolutely necessary if, for example, you ever have to apply for financing.

One of the features of accounting systems you should understand is the Chart of Accounts. You won’t have to alter it in any way—in fact, we strongly advise against it—but you’ll encounter it when you work with transactions. Here are five things you should know about it. What is it?

These three columns from QuickBooks Online’s Chart of Accounts display account Names, Types, and Detail Types.

QuickBooks Online’s Chart of Accounts is a list of financial categories that are used to classify your company’s transactions when you record them. If you were doing your accounting manually, you would have to create your own Chart of Accounts. But QuickBooks Online builds one for you based on the company type and industry you choose when you’re setting up the site.

Why is the Chart of Accounts important?

Some people refer to the Chart of Accounts as the “backbone” of your company file. All transactions flow to it. Its primary importance can be summed up in one word: reports. Your reports will not be accurate if your Chart of Accounts is poorly constructed or if you categorize transactions incorrectly. This becomes as issue when you want to:

- Prepare taxes. Your income tax return will not reflect your reportable income and deductible expenses if transactions are not assigned to the right classifications.

- Apply for financing, take on an investor, sell your company, etc.

- Monitor your finances. You won’t get a true picture of your income and expenses, which makes it difficult to analyze your company’s fiscal health and plan for the future.

What’s in the Chart of Accounts?

There are two types of accounts. One contains information that’s used in the Balance Sheet report. These accounts will have a number in the QuickBooks Balance column that’s based on all transactions up to the current date. They include Assets (bank accounts, accounts receivable, inventory, etc.), Liabilities (unpaid bills, credit cards, payroll and sales taxes, loans, etc.), and Equity.

The remainder of the accounts are used in the Profit and Loss report, otherwise known as the Income Statement. They’re divided into Income (sales, discounts given, etc.), Cost of Goods Sold (labor, shipping, materials and supplies, etc.), Expenses (advertising, insurance, payroll, etc.), Other Income, and Other Expense. You won’t see a number in the QuickBooks Balance column for these accounts because the Profit and Loss report changes based on the date range selected.

Should I ever make any modifications to my Chart of Accounts?

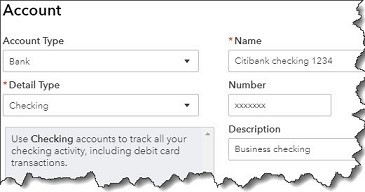

You can set up bank and credit card accounts in QuickBooks Online’s Chart of Accounts.

As we stated earlier, we strongly recommend that you never modify your Chart of Accounts without consulting us. However, there are two exceptions to this. You’ll want to create entries for your bank and credit card accounts. To do this, first open the Chart of Accounts by clicking the gear icon in the upper right and selecting Chart of Accounts under Your Company. When it opens, click New in the upper right corner. Choose Bank or Credit Card and fill in the blanks.

Do I need to use account numbers in the Chart of Accounts?

Generally, the smaller the business, the less need there is for this. If your business is big enough that you have dedicated A/P and A/R individuals, you may want to post transactions to account numbers.

Understanding Reports

QuickBooks Online makes it possible for you to view the Chart of Accounts and those two critical reports, Balance Sheet and Profit & Loss. Customizing and analyzing them, though, is something you should do under professional supervision. We’re happy to help here and in other advanced areas of the site. Contact us for a consultation.