Categories for

Understanding the Weighted Average Cost (WAC) Method for Inventory Valuation

When it comes to businesses and their inventory and accounting methods for managing it, there are a few different ways to approach the task. The three different options to value inventory/implement cost flow assumptions include Last In, First Out (LIFO); First In, First Out (FIFO); and Weighted Average Cost Accounting (WAC). This article will focus only on the WAC method.

Weighted Average Cost (WAC) Method

WAC is a way to value inventory based on how much each tranche contributes to the overall valuation of its cost of goods sold (COGS) and inventory. Recognized by both GAAP and IFRS, it’s determined by taking the cost of goods available for sale and dividing it by the quantity of inventory ready to be sold. It’s important to note that while WAC is a generally accepted accounting principle, it’s not as precise as FIFO or LIFO; however, it is effective at assigning the average cost of production to a given product.

It’s done primarily for types of inventories where parts are so intertwined that it makes it problematic to attribute clear-cut expenditures to a particular part. This often happens when stockpiles of parts are indistinguishable from each other. It also accounts for businesses offering their inventory for sale all at once. Here’s a visual representation of the formula:

Weighted Average Cost (WAC) Method Formula

WAC per unit = Cost of goods available for sale / Units available for sale

Costs of goods available for sale are determined by adding new purchases of inventory to the value of what the business already had in its existing stock. Units available for sale are how many saleable items the company possesses. Its value is assessed per item and encompasses starting inventory and additional purchases.

When it comes to calculating WAC, there are two different types of inventory analysis systems: periodic and perpetual.

Periodic Inventory System

In this system, the business tallies its inventory at the end of the accounting period – be it a quarter, half, or fiscal year – and analyzes how much the inventory costs. This then determines the value of the remaining inventory. The COGS is then calculated by adding how much starting, final, and additional inventory within the accounting period cost.

Perpetual Inventory System

This system puts a bigger emphasis on more real-time management of its stock levels. The trade-off for such real-time tracking of inventory requires more company financial resources. Looking at an example of how a company began its fiscal year with the following inventory can illustrate how it works.

At the beginning of the year, the company had 1,000 units, costing $50 per unit. It also made three additional inventory purchases going forward.

Jan 20: 75 units costing $100 = $7,500

Feb 17: 150 units costing $150 = $22,500

March 18: 300 units costing $200 = $60,000

During the fiscal year, the business sold:

235 units sold during the last week of February

325 units sold during the last week of March

Looking at the Periodic Inventory System, for the first three months of its fiscal year, the company can determine its COGS and the number of items ready to be sold over the first three months of its fiscal year.

WAC per item – ($50,000 + $7,500 + $22,500 + $60,000) / 1,525 = $91.80

Based on this method, the WAC per unit would be multiplied by the number of units sold during the accounting period, therefore:

560 units x $91.80 = $51,408 (inventory sold)

To calculate the final inventory value, we take the entire purchase cost and subtract the remaining inventory to arrive at the valuation:

$140,000 – $51,408 = $88,592

Perpetual Inventory System

Unlike the periodic inventory system, this looks at determining the mean prior to the transaction of items:

This would calculate the average before the 235 units were sold during the last week of February:

WAC for each item: ($50,000 + $7,500 + $22,500) / 1,225 = $65.31

Looking at the 235 units sold during the last week of February, it’s calculated as follows:

235 x $65.31 = $15,347.85 (inventory sold)

$80,000 – $15,347.85 = $64,652.15 (remaining inventory value)

Before calculating for the 325 units sold the last week of March, the unit valuation per WAC is: ($64,652.15 + $60,000) / (1225 – 235 + 300) = 1290 = $96.63

Looking at the 325 units sold during the last week of March are calculated as follows:

325 x $96.63 = $31,404.75 (inventory sold)

$124,652.15 – $31,404.75 = $93,247.40 (remaining inventory)

Based on these options, businesses have the choice, along with LIFO and FIFO, to decide how they want to vary it based on their own business needs.

Save Time, Keystrokes with Recurring Transactions in QuickBooks Online

Accounting takes time. And the last thing you need when you’re working with your company’s finances is an activity that takes unnecessary minutes. If you’ve created a record or transaction once, you don’t want to have to enter the information a second or third time.

That’s why using QuickBooks Online is so far superior to manual accounting. It remembers everything, so you can use data again when you need it. But sometimes you have to give it a little guidance.

That’s the case with recurring transactions. If you have forms that you create repeatedly, with very few changes (like utility bills), you can “memorize” the transactions. When the bill comes around the next month, you can modify any details necessary and dispatch it again. Here’s how it works.

Three Options

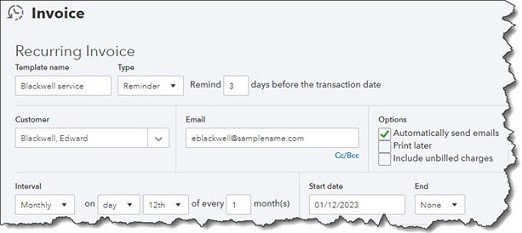

To get started, enter a transaction that you want to save and be able to use again (with changes). Let’s say it’s an invoice that you send to a customer once a month who has a service contract for network maintenance. When you’ve completed the form, look toward the bottom of the screen and click Make recurring. The screen will now read Recurring Invoice, with new content as pictured below.

You can specify transactions as recurring and add details like frequency and start/end dates.

If you want to change the Template name to something that will remind you of its purpose, you can do so. In the field beneath Interval, select Daily, Weekly, Monthly, or Yearly, and then indicate what day of the month the transaction should occur. Enter a Start date and End [date] or select None if the length of service is open-ended. In the example above, you would receive a reminder from QuickBooks Online three days before the invoice is scheduled to go out. The service contract has no ending date, so you’d continue to get reminders until you change the template.

Next to the Template name is a field labeled Type. QuickBooks Online gives you three options for taking action on recurring transactions. It can be:

- Scheduled. This is an automated option that should be used with caution. If you select this, your transaction will go out as scheduled with no intervention from you. Only the date will change.

- Reminder. QuickBooks Online will send you a reminder ahead of the scheduled date. You can specify how many days ahead you should receive it. Then it’s up to you to make any necessary changes and send it out.

- Unscheduled. QuickBooks Online will do nothing except save your template.

When you’ve completed all of the required fields, click Save template in the lower left.

Using Recurring Transactions

If you’ve chosen the Scheduled option for any transactions, you don’t have to do anything more with it until you want to change its content or status. To find your list of recurring transactions so you can process any that are earmarked as Reminder or Unscheduled, click the gear icon in the upper right of the QuickBooks Online screen. Under Lists, click Recurring transactions.

The Recurring Transactions table

The screen that opens displays a table containing all of your recurring transactions. You can learn just about everything you need to know about those transactions here: Template Name, Type, Txn (Transaction) Type, Interval, Previous Date, Next Date, Customer/Vendor, and Amount.

The last column in the table, labeled Action, opens a menu that displays different options depending on the type of transaction. For our Reminder example, you can:

- Edit (edit the template, not the transaction)

- Use (opens the original transaction that you can edit, save, and send)

- Duplicate (duplicate the template)

- Pause (stop sending reminders temporarily)

- Skip next date

- Delete

Looking Ahead

We’re a month into 2023 now. What does this year look like for you? Is QuickBooks Online doing everything you need it to do? If you’re starting to outgrow your version, we’d be happy to consult with you about upgrading to another service level (Essentials, Plus, or Advanced). Or if you know the version you’re using is supposed to do something you need but can’t quite figure it out, let us know. We want 2023 to be a good year for you, and we’d like to make your accounting work as painless and productive as possible.

The Implications of the R&D Tax Policy Changes on Manufacturers Everywhere

If you’ve been keeping up with the news, you’re no doubt aware of a recent policy change that will impact the way that research and development (R&D for short) is handled when it comes to income taxes in the United States. Rather than being allowed to deduct those costs immediately, companies are now being told that they must spread those costs out over a period of five years.

Unsurprisingly, those companies are none too thrilled with that change. It has the potential to hurt manufacturers in a number of different ways, all of which are worth exploring.

The R&D Tax Policy Change: An Overview

In a letter that was sent on November 4, 2022, no less than 178 CFOs – primarily those from some of the biggest names in United States manufacturing like Ford Motor Company, Lockheed Martin, Boeing, and others – outlined why they believe that these aforementioned new rules would lead to what they call a “competitive disadvantage” for American companies. This in turn would almost certainly lead to job losses, which would in turn harm their ability to innovate over the next decade.

Their point of view was simple: they were asking the current Congress to switch back to a system that allowed them to immediately deduct their costs when it came to research and development as soon as the end of the year.

It’s important to note that in a general sense, research and development investment does not spread evenly across the economy. It tends to be heavily localized in a few key spaces, with manufacturing being chief among them. In fact, the manufacturing sector alone accounts for 58% of all research and development costs according to one recent study.

To contextualize that in a different way, it means that the manufacturing sector would face a significant tax increase as per the research cited above – to the tune of $31.7 billion in 2023 alone which is directly attributed to this new approach to R&D amortization.

It’s equally important to note that, until January 1, 2022, businesses could deduct 100% of all expenses that were directly attributed to research and development in the same year that they were incurred. On January 1, 2023, on the other hand, this new law goes into effect. This essentially makes it not only more expensive to invest in advancements that will help innovate various sectors like manufacturing, but in the growth of these companies as well.

Many agree that this means that the sector won’t just get hit, it will get hit significantly. This is essentially a major new expense – the fact that the tax liabilities of these companies are about to increase exponentially – that was not anticipated up to this moment.

One company that is particularly worried about the implications of this change is Miltec UV. Right now, company leadership believes that an exciting new opportunity is within reach. They have spent years developing a new technology for lithium-ion batteries – otherwise known as the rechargeable batteries that are found in countless devices like your smartphone or tablet. This new technology could potentially be used for next-generation electric vehicles.

Miltec UV has poured no less than 11 years of development into manufacturing the electrodes that will be used in these batteries. They’ve spent countless amounts of money on prototyping. There has been various proof of concepts developed to indicate that these microbes can do what the company thinks they can. There has been testing. On top of it all, there is the cost to manufacture the batteries. Officials agree that they are very close to the point where they can commercialize the batteries and begin to sell them, but with these new rule changes that also means that they will have to pay more taxes than they previously thought they would.

In the event that these tax changes are not reversed, industry leaders fear that they will hurt profits in the short term. This could then negatively impact essential benefits that employees at manufacturing companies have come to count on.

For the record, Miltec UV is also an organization that funds all of its research and development efforts through the profits of its various commercial businesses. It has eschewed taking on outside investment in the past and hopes to continue to do so moving forward.

Regardless of whether Congress reverses these changes, one thing is for certain – this is a development that the entirety of the manufacturing industry will be paying close attention to moving forward.

Planning On Buying a New Electric Vehicle and Claiming a Tax Credit? Better Read This First

Although the credit for purchasing a new electric vehicle can still be as much as $7,500, Congress has added some new stringent qualifications as to which vehicles qualify, and for the first time, Congress has limited who qualifies for the credit by barring the credit to higher income taxpayers.

But first a little background. Prior to this change, a vehicle qualifying for the credit needed only to be a 4-wheel vehicle, with a minimum battery capacity of 5-kilowatt hours and a gross weight of less than 14,000 pounds. There was also a manufacturer limit of 200,000 units, after which the credit phased out over the subsequent four quarters. There were no qualification requirements for the purchaser of the vehicle.

New Qualifications – Under the new law, starting in 2023 the vehicle and the buyer must meet far more stringent requirements for a taxpayer to qualify for the clean vehicle tax credit.

Purchaser’s Income Limit – No credit is allowed for any tax year if the lesser of the modified adjusted gross income (MAGI) of the buyer for the:

- Current tax year, or

- The preceding tax year exceeds the threshold amount as indicated below. There is no phaseout and just one dollar over the limit means no credit will be allowed. Thus, Congress has essentially eliminated the credit for higher-income taxpayers.

- Married Filing Joint or Surviving Spouse – $300,000

- Head of Household – $225,000

- Others – $150,000

MAGI is the buyer’s adjusted gross income increased by any foreign earned income and housing exclusions and excluded income from Guam, American Samoa, the Northern Mariana Islands, and Puerto Rico.

Vehicle Qualifications – To qualify, the vehicle must:

- Be a 4-wheel vehicle.

2. Be a Street Vehicle that was manufactured primarily for use on public streets, roads, and highways.

3. Have a Minimum Battery Capacity of 7 kilowatt-hours.

4. Be acquired for Original Use by the taxpayer. Original use means that the vehicle has never been used by any taxpayer for any purpose. A vehicle is not a new clean vehicle if another person has ever purchased or leased the clean vehicle and placed it in service for any purpose. Where a vehicle is acquired for lease to another person, the lessor is the original user.

5. Have had its Final Assembly in North America, which includes the 50 states, the District of Columbia, and Puerto Rico, Canada, and Mexico. Where the vehicle was manufactured can be determined from the 17-digit vehicle identification number (VIN). The VIN Decoder website for the National Highway Traffic Safety Administration (NHTSA) also provides final assembly location information. The website, including instructions, can be found at VIN Decoder.

The VIN is permanently attached to a vehicle in several locations, appearing on the dashboard for most passenger vehicles and on the label located on the driver’s door frame. The VIN is also located on the window sticker of new vehicles and often appears on the vehicle listing on dealers’ websites.

- Meet the MSRP requirement – The manufacturer’s suggested retail price (MSRP) cannot exceed:

- $80,000 for vans, SUVs, and pickups

- $55,000 for other vehicles

The MSRP will be on the vehicle information label attached to each vehicle on a dealer’s premises. The MSRP for this purpose is the base retail price suggested by the manufacturer, plus the retail price suggested by the manufacturer for each accessory or item of optional equipment physically attached to the vehicle at the time of delivery to the dealer. It does not include destination charges or optional items added by the dealer, or taxes and fees.

Even when a vehicle is purchased for less than the MSRP, the credit limitation on the price of the vehicle is based on the manufacturer’s suggested retail price (MSRP), not the actual price paid for the vehicle.

- Meet the Critical Mineral and Battery Components test – Congress, in an effort to bring the battery manufacturing for electric vehicles to the United States, included a requirement that a percentage of critical minerals needed to manufacture batteries be extracted or processed in the U.S. or a country with a free trade agreement with the U.S. or recycled in the U.S. It also requires a percentage of battery components be manufactured or assembled in North America. The initial percentage is 50% and 100% after 2028.

Luckily for a buyer, the dealer must provide a report that certifies the vehicle meets these requirements by specifying the amount of credit the vehicle qualifies for.

Seller Provided Report – The seller of the vehicle is required to furnish a report to the buyer and the IRS that includes:

- The name and taxpayer identification number of the buyer;

- The vehicle identification number (VIN) of the vehicle (it will be required on the tax return to claim the credit), unless, by U.S. Department of Transportation rules, the vehicle is not assigned a VIN;

- The battery capacity of the vehicle;

- Verification that the original use of the vehicle commences with the taxpayer; and

- The maximum Clean Vehicle Credit allowable to the buyer with respect to the vehicle.

List of Qualifying Vehicles – The IRS provides a list of eligible vehicles on its website.

Transfer of Credit to the Dealer – After 2023, the taxpayer purchasing the vehicle, on or before the purchase date, can elect to transfer the clean vehicle credit to the dealer from whom the vehicle is being purchased in return for a reduction in purchase price equal to the credit amount.

A buyer who has elected to transfer the credit for a new clean vehicle to the dealer and has received a payment from the dealer in return, but whose MAGI exceeds the applicable limit, is required to recapture the amount of the payment on their tax return for the year the vehicle was placed in service.

If you have questions about these new rules on the clean vehicle credit, please give our office a call.

Start Off on the Right Foot for the 2023 Tax Year

Individuals and small businesses should consider various ways of starting off on the right foot for the 2023 tax year.

W-4 Updates – If you are employed, then your employer takes the information from your Internal Revenue Service (IRS) Form W-4 and applies it to the IRS’s withholding tables to determine the amount of income tax to withhold from your wages in each payroll period.

If your 2022 refund or balance due turns out not to be the desired amount, you may want to consider adjusting your withholding based on your projected tax for 2023. If you need assistance, please call this office.

W-9 Collection – If you are operating a business, then you are required to issue a Form 1099-NEC to each service provider to which you have paid at least $600 during a given year. It is a good practice to collect a completed W-9 form from every service provider (even if you are paying less than $600), as you may use that provider again later in the year and may have difficulty getting a W-9 after the fact—especially from providers that do not plan to report all of their income for the year.

Estimated Tax Payments – If you are self-employed, then you prepay each year’s taxes in quarterly estimated payments by sending 1040-ES payment vouchers or making electronic payments. For the 2023 tax year, the first three payments are due on April 18, June 15, and September 15, 2023, and the final payment is due on January 16, 2024. Generally, these payments are based on the prior year’s taxable income; if you expect any significant changes in either income or deductions relative to the previous year, please contact this office for help in adjusting your payments accordingly.

Charitable Contributions – If you marginally itemize your deductions, then you can employ the bunching strategy, which involves taking the standard deduction one year but itemizing your deductions in the next. However, you must make this decision early in the year so that you can make two years’ worth of charitable contributions in the bunching year.

Required Minimum Distributions – Each year, if you are 73 (a recent law change increased it from 72 in 2022) or older, you must take a required minimum distribution from each of your retirement accounts or face a substantial penalty. By taking this distribution early in the year, you can ensure that you do not forget and accidentally subject yourself to penalties.

Gifting – If you are looking to reduce your estate-tax exposure or if you just want to give some money to family members, know that each year, you can gift up to an inflation-adjusted amount, which for 2023 is $17,000, to each of an unlimited number of beneficiaries without affecting your lifetime estate-tax exclusion amount or paying a gift tax.

Retirement-Plan Contributions – Review your retirement-plan contributions to determine whether you can afford to increase your contribution amounts and to make sure that you are taking full advantage of your employer’s contributions to the plan.

Beneficiaries – Marriages, divorces, births, deaths, and even family clashes all affect whom you include as a beneficiary. It is good practice to periodically review not just your will or trust but also your retirement plans, insurance policies, property holdings, and other investments to be sure that your beneficiary designations are up to date.

Reasonable Compensation – With the advent a few years ago of the 20% pass-through deduction, which is available to most businesses other than C-corporations, the issue of reasonable compensation took on new importance, particularly for shareholders of S corporations. This has been a contentious issue in the past, as it has allowed shareholders who are not just investors but who are actually working in the business to take a minimum salary (or no salary at all) so that all their income passed through the K-1 as investment income. This strategy allows such shareholders and the S corporation to avoid payroll taxes on income that should be treated as W-2 compensation. A number of issues factor into a discussion of reasonable compensation, including comparisons to others working in similar businesses and to employees within the same business, as well as the cost of living in the business’s locale. This is a subjective amount, and it generally must be determined by a firm that specializes in making such determinations.

Business-Vehicle Mileage – Generally, vehicles with business use also have some amount of nondeductible personal use in a given year. It is always a good practice to record a vehicle’s mileage at the beginning and at the end of each year so as to determine its total mileage for that year. The total mileage figure is then used when prorating the personal- and business-use expenses related to that vehicle.

College-Tuition Plans – Contribute to your child’s Section 529 plan as soon as possible; the funds begin accumulating earnings as soon as they are in the account, which is important because the student will likely begin using that money at age 18 or 19.

Only a few of the tax-related actions that you take during a year will benefit yourself or others. The most important of these actions is keeping timely and accurate tax records; for businesses in particular, this is of the utmost importance. Those who have well-documented income and expense records generally come out on top when the IRS challenges them.

If you have any questions related to your taxes or if would like an appointment for tax projections or tax planning, please contact our office.

401(k) Options After You Leave an Employer

Apart from the spike in inflation, 2023 ended the year with a relatively strong economy, boasting an unemployment rate of 3.5 percent (below the market forecast of 3.7 percent) with increases in wages, corporate profits, and economic growth over the past two quarters. Despite the positive data, a slate of companies including Microsoft, Google, Amazon, Goldman Sachs, and Bed Bath & Beyond have all announced significant layoffs planned for this year.

Whether the result of a layoff, a new job, or retirement, the reality is that throughout a career, most people will change jobs several times. The good news is that 401(k) plan assets are portable – meaning you can take them with you. However, it is important to be aware of all your options so that you choose the most advantageous one each time you change employers.

You Don’t Have to do Anything Right Away

The first thing to note is that the income deferrals you contributed to your employer’s retirement plan are yours to keep. However, an employer match may be subject to a vesting schedule. If you do not work at the company long enough to satisfy the vesting schedule, you might lose all or a portion of the unvested assets in your account.

It is not necessary to roll over your 401(k) assets right away; in many cases, you can leave them where they are indefinitely. However, you will no longer be able to make contributions to the plan, receive matching funds, or tap that money for a loan. If the plan has a wide range of investment options, low fees, and expenses and has performed well, then leaving assets where they are may be your best choice.

On the other hand, you should investigate to ensure your plan does not change once you no longer work for a former employer, as some plans charge higher fees for inactive employees. Also, some employers may require you to cash out of your account balance – usually if it is below $1,000. If your balance is above $1,000, that employer must offer you the option to roll those assets into a personal IRA.

Take the Money

If you opt to withdraw the cash value of your account, you will be subject to an immediate tax impact. Your company may cut you a check for the amount withdrawn, but it is required to withhold 20 percent of the amount to prepay the tax you’ll owe. If you have not yet reached age 59½, the IRA will classify the distribution as an early withdrawal. This means you might owe a 10 percent penalty in addition to the federal tax withholding. The balance also may be subject to state and local taxes. All told, you could lose up to 50 percent of the account value if you take an early distribution.

For young adults in particular, it can be tempting to withdraw their 401(k) balance when they leave an employer. They may not have acquired much in assets, not met vesting requirements for the employer match, and figure they have more need for the money now than in 50 years when they retire. However, bear in mind that investments made early as an adult often purchase good, dependable stocks at low prices, with decades for those stocks to appreciate. Holding onto those assets over the long term allows for maximum growth opportunity, whereas withdrawing them means you’ll have to start all over again.

Roll Over Assets to Your New Employer’s 401(k)

Some employer plans will accept transfers from a former retirement plan, but not all of them do. You will have to inquire. If this is an option, recognize that there is no need to roll over right away. You may want to work there for a while to ensure you’re happy, the company is viable, and you plan to stay there for a while. Furthermore, you may have to wait until the next enrollment period to request a rollover, and some employers may require that you work a specific period of time (e.g., one full year) before you can transfer old 401(k) assets to your new plan.

Open a Personal IRA

A third option is to transfer your old employer’s 401(k) assets to a personal individual retirement account (IRA) that you open through a brokerage of your choice. The new brokerage custodian will give you the forms needed to request the formal rollover, and your former 401(k) plan administrator might have forms to complete as well. It is best to have the two custodians conduct the transfer directly so that you never take possession of the funds yourself, which could result in tax penalties if not conducted correctly.

You’ll need to select new investment options (e.g., mutual funds, exchange-traded funds, individual stocks or bonds) for the IRA, and be sure to compare its fees with your old account. By rolling over to an IRA that you manage yourself, you will have a wider range of investment options and can shop for plans with lower fees.

Bear in mind that, moving forward, any additional contributions you make to this IRA will be subject to lower annual contribution limits (in 2023: $6,500 if under age 50; $7,500 for 50 and older) than 401(k) plans, as well as the income limitations applicable to a Roth IRA (2023: less than $153,000 Modified Adjusted Gross Income (MAGI) if you are single; less than $228,000 if you’re married and file jointly).

There are three IRA rollover options for 401(k) plan assets:

- Roll over to a new or existing traditional IRA – No taxes are due on the assets you transfer and earnings continue to accumulate tax deferred until withdrawn. It’s best to directly roll over the funds from one custodian to another.

- Roll over to a new or existing Roth IRA – This option requires that you pay taxes on the rollover amount in the tax filing year they are transferred. You may use money from the 401(k) plan or pay the tax separately using other assets (the latter is preferable so that your equity continues to appreciate). Once the IRA has been open for at least five years and you are at least age 59½, contributions and earnings can be withdrawn free of all taxes and penalties. Furthermore, unlike the traditional IRA, you are not required to take minimum distributions (RMDs) from a Roth.

- Roll over a Roth 401(k) to a new or existing Roth IRA – No taxes are due when the money is transferred and new earnings accumulate tax deferred. Contributions and earnings are eligible for tax-free withdrawals once the IRA has been open for at least five years and you are at least age 59½.

Do Something

Leaving your 401(k) with a former employer is a perfectly acceptable option, but you should consider consolidating your 401(k) plans at some point. More and more people are working for multiple employers throughout their careers, and they may lose track of where they hold 401(k) assets. In fact, at the end of 2021, there was a nationwide total of $1.35 trillion sitting in forgotten 401(k) plans.

Don’t let that happen to you.

Defining an Impaired Asset

When it comes to defining an impaired asset, its fair market value is worth less than the original cost of the asset – or more formally, its carrying value. As a company re-evaluates its assets’ value, and when it determines there’s a discrepancy between the book or original value and the current market value, impaired assets that are lower in value are written down on the balance sheet. The business’ income statement shows a loss for the negative difference in value. Impaired assets can be Property, Plant, and Equipment (PP&E), goodwill, or fixed assets.

Making a Judgment on Asset Impairment

One more consideration to get an accurate calculation, according to generally accepted accounting principles (GAAP), is to ensure that accumulated depreciation is subtracted from the asset’s historical or original cost before assessing the difference between the fair market and carrying values. Equally as important is the GAAP recommendation for businesses to perform impairment tests annually.

Assets could be damaged physically, consumer demand may change, or legal factors could reduce their fair market value. These reasons may cause lowered projected future cash flows – lower than an asset’s current carrying value. It, therefore, requires an impairment assessment.

Illustrating With a Real-World Example

Take a business that bought a piece of equipment 24 months ago worth $500,000 and depreciates at $25,000 annually. Using these two figures, we can determine the equipment’s carrying value as follows for the present year:

[($500,000 – ($25,000 x 2 years)] = $450,000

If the same type of asset (same age, usage, etc.) can be purchased on the open market but is able to be purchased for $400,000 (market value), the asset the business owns would be considered an impaired asset.

The difference between the current market value and the carrying value is $450,000 – $400,000 = $50,000. The $50,000 would be written down.

It’s important to note that once an asset is impaired, depreciation going forward must be recalculated based on the new valuation figure.

Criteria to Establish Impairment

According to GAAP, businesses must begin with a recoverability test. If the initial cost of an asset (minus any depreciation or amortization) is more than the non-discount rate adjusted cash flows it’s projected to produce, the asset is considered impaired.

Assuming the asset is deemed impaired, the second part determines how much impairment exists, which is the gap between the original and market value of the asset in question. If the fair value is unspecified, the total of the discount rate adjusted future cash flows are acceptable.

Assuming the total of non-discount rate adjusted future cash flows is $90,000 – the projected undiscounted cash flows through the next 36 months, which is lower than the estimated carry amount (or book value) of $115,000. The recoverability test is passed, so the asset should be impaired. Based on the second step, the impairment loss will be $25,000 ($115,000 – $90,000). If, however, the fair market value is unknown, the projected cash flows of $30,000 per year for the next 36 months should be discounted to present value. This example can assume a 5 percent discount rate:

Year 1 – $30,000 / (1+0.05) = $30,000 / 1.05 = ($28,571.43)

Year 2 – $30,000 / (1+0.05)^2 = $30,000 / (1.1025) = ($27,210.88)

Year 3 – $30,000 / (1+0.05)^3 = $30,000 / (1.1576) = ($25,915.69)

To calculate the impairment loss with an unknown fair market value: $115,000 – ($28,571.43 + $27,210.88 + $25,915.69) = $115,000 – $81,698.00 = $33,302.00

Whether it’s a time of economic uncertainty or the economy is firing on full cylinders, assets can change value. Businesses that effectively navigate changing conditions are able to increase their chances of surviving or thriving amid the challenges they might face.

End of Life Planning: 5 Steps to Take in 2022

End-of-life planning is a delicate—but incredibly important—subject. While contemplating your own death and the fallout thereof probably feels morbid, making preparations for your passing is an incredible way to demonstrate your love to those near and dear to you. Taking the time to plan for some of the logistical details surrounding your death can go a very long way in lightening the heavy load that your loved ones will bear.

Whether you already have your end-of-life plan established or you have yet to do so, there is still work to do. Today we want to address 5 key areas that you should examine in 2022 in order to establish or strengthen your end-of-life plan.

1. Incapacitation – Your desires regarding how healthcare decisions are made in the event of your incapacitation

To establish, partner with an attorney to create your living will. Be sure that you establish power of attorney with a loved one in the event of your incapacitation.

To maintain, review your living will and update your power of attorney to reflect any changes

2. Inheritance – Your plan for how your valued assets will be passed on after your death

To establish, once again, find an attorney who is well versed in estate law. Work with them to create your will.

To maintain, review the will that you have already created, updating it for any major life changes that have bearing on it. Some examples of important changes that might require updates include an increase in your wealth, the birth or death of a loved one, or new marriages or divorces.

3. Information – A record of your papers, accounts, passwords, and more

To establish, make a thorough record of all of the key information that your loved ones and/or legal representatives might need after you pass on. This includes personal information, family information, important contacts, the location of important papers, funeral and interment details, obituary information, login and password information, social media account information, copies of important documents, and more.

To maintain, review the record that you have created and make any changes required to maintain its accuracy and relevance.

4. Dependents – Your plan for the continued care of any minor children, adult dependents, and/or pets

To establish, make a thorough plan that covers the care of any and all dependents that your death or incapacitation would leave hanging. It is best to work with an attorney in order to make sure all of your bases are covered.

To maintain, review the dependent care plan that you have already created, updating it for any major life changes that have bearing on it. Consider checking in with any individuals whom you have named to care for your dependents to make sure that they are still willing to be included in your plan.

5. Tax Planning – Your strategy for minimizing the taxes and expenses associated with the passing on of your estate

To establish, regardless of the size of your estate, having a clear plan in place is an important part of end-of-life planning. There are a number of key financial planning steps you can take in order to make the burden that your loved ones will carry as light as possible. We strongly recommend working with a tax accountant to make a thorough plan that minimizes the taxes and expenses that your loved ones will face in the event of your death.

To maintain, be sure to review your plan with your tax advisor on a regular basis in order to make sure that it is still optimized for your situation.

Taking the time to make and maintain a thorough end-of-life plan is one of the best gifts you can leave your loved ones upon your passing. It is a hard topic to address, but an incredibly important one.

Though this article offers some helpful tips and starting points, the best way to create a thorough and effective end-of-life plan is to work with a professional who can guide you each and every step of the way. If you are ready to take this important planning step, reach out to the RBG professionals today. You can do so via our website’s Contact page or by emailing rbfco@rbfco.com. Be sure to request a copy of our free “Everything They Need to Know” digital planning guide.

Why You Might Not Need a New Budget for the New Year

So, we’re a month into 2023 and the sheen might’ve dulled from all your shiny, New Year’s resolutions. Though diet and exercise are the top things you might want to change, there’s one you might not need to touch – your budget. Here’s a discussion about who does and doesn’t need to revamp their finances.

Who Needs a New Budget?

Budgets are always a good idea. They help you save money and pay off debt. But only a few folks need to create a new one. According to Annette Harris, founder of Harris Financial Coaching, you need a new budget if you are:

- Unable to keep up with expenses

- Falling behind on debt payments

- Borrowing money from others

- Relying on credit cards

- Using payday lenders

But on the flipside, some positive life events may also call for a fresh look at your budget:

- Buying a house

- Planning home improvements

- Sending a child to college

Now, if you’re debt-free, saving and investing, then a new budget probably won’t provide much value. Further, Harris says that if you don’t have children that you’re putting through college, don’t have any upcoming big purchases, continue to spend wisely and build your net worth, don’t bother changing what you’re already doing. In other words, of it’s not broke, don’t fix it.

The Stigma Around the ‘B’ Word

That would be “budget.” Jesse Mecham, founder of the app You Need a Budget aka YNAB, has a good explanation about why this is so. He says that this very term (budget) is among the reasons that people don’t follow through with setting one – and sticking with it. He says that generally, people think it means restriction, deprivation or diet. What you need, he says, is a shift in perspective. If you think about a budget being a plan for intentional spending, no matter what year it is, you always want to be intentional. Makes good sense, right?

Some Budgets Might Even Cause Harm

Dana Miranda, founder of the “budget-free” financial ed website Healthy Rich, believes that budgets can do more harm than good. She says that people inevitably feel like they’re failing and aim for a fresh start at the beginning of the year; but no amount of recommitting to budgeting can make the realities of your life fit into the unrealistic restriction of a budget. Miranda says when people are stressed about money, they budget. When they succeed, it’s great. But when they fail, they feel like a failure and, consequently, are even more stressed. Much like dieting.

Alternatives to Budgeting

Here are three other ways to get a handle on your finances in the New Year.

Track Your Goals

We’re not talking about counting every dollar, but focusing on goals. Instead of not overspending, eating out less or avoiding online shopping, find areas in your budget that can help you accomplish your goals – one at a time. For instance, if you want to save for college for your kids, buy an investment property, or create a vacation fund, set up a tracker with a defined timeline and work toward that. It’s easier to narrowly focus on one important goal than on everything all at once.

Create an Annual Budget

This is in contrast to a monthly budget. This helps you accommodate for variables – life stuff – that inevitably come your way and knock you off course. According to Harris, take time to map out monthly costs, travel plans, and home renovations, along with any one-time and variable recurring costs. The bills you pay regularly are easy to anticipate; it’s the ones you don’t that will throw you a curveball.

Look at Your Relationship With Money

Ask yourself things like:

- Do I find joy in the way I make money?

- Are the commitments I made (like a monthly savings amount) still working for me?

- Am I achieving what I want?

- Am I at peace with the way I spend?

Harris says self-awareness found through journaling, meditation, yoga, and prayer are great ways to harness conscious spending. They contribute, she says, to helping you become more intentional with the way you spend.

No one is perfect. Everyone makes mistakes. However, with a few helpful hints like these, you can get better and better every day.

Sources

https://www.forbes.com/advisor/personal-finance/new-budget-new-years-resolution/

2022 Consumer Saving & Spending Behaviors (bankofamerica.com)

Handling Talent Shortages in Tech Departments

Technology advancement has brought about great digital transformation. Unfortunately, this has come with a global tech talent shortage. IT executives highlight the shortage as a huge barrier to the adoption of emerging technologies, as reported by this Gartner study.

It is estimated that the demand for tech talent will keep increasing, and this could result in an estimated 85 million global talent shortage by the year 2030. Therefore, companies need to rethink their approach to hiring and retention.

Reasons Behind the Tech Talent Shortage

It is worth trying to first understand what is causing the tech talent shortage. A few of the reasons that have led to the shortage include:

- Advances in technology – Technology is advancing at a high speed, requiring workers with skills to match the new technology. Unfortunately, the tech education system can’t keep up with the speed, hence a shortage of people with the required skills.

- The great resignation – This became a buzzword with work from home that came with the Covid pandemic; unfortunately, even after the pandemic, people are still leaving their jobs. A survey by TalentLMS and Workable found 72 percent of employees working in tech are considering quitting their jobs or exploring other opportunities.

- High demand for tech talent – There has been an increase in the demand for tech workers in recent years as more businesses and industries turn to technology for daily operations. New technology creates new roles such as data professionals, data security specialists, and software engineers among others that are highly competitive.

- Challenges in training and development – some companies might not have the resources and time to invest in employee development.

Business Challenges of IT Talent Shortage

Businesses are feeling the effect of the tech talent shortage, especially when it comes to digital transformation. Emerging technologies such as robotic process automation (RPA), artificial intelligence, blockchain and augmented reality that promise to keep a business ahead of its competition require skilled workers.

Hiring new talent or reskilling employees also comes at a cost, and companies struggle to fill positions. On the other hand, failing to have skilled employees results in unrealized annual revenues.

As a result, businesses of all sizes find themselves failing to develop projects on time and hence fail to meet deadlines. In other cases, the existing employees end up overburdened with too much work, and this may lead to them quitting. Eventually, a business experiences slow innovation and slow growth.

How to Handle the Tech Talent Shortage

A few strategies to help address this issue include:

- Investing in employee development and training

Providing ongoing training and development opportunities for current employees can help them acquire new skills and knowledge. This will not only make them more valuable to your organization, but also less likely to leave.

- Attract top talent through a strong employer brand

Building a strong employer brand can help in attracting top talent to your organization. This can involve highlighting your company’s culture, values, and mission, as well as offering competitive compensation and benefits packages. A good reputation will also help attract new talent.

- Partnering with educational institutions

A company may also partner with local colleges and universities to gain access to a pool of talented students who are looking for internships or entry-level positions. Additionally, setting up mentorship or internship programs helps build a pipeline of talent for your organization.

- Increase recruitment efforts

Sometimes it might be difficult to find the right talent, which makes it necessary to increase recruitment efforts. This could involve working with recruitment agencies, posting job openings on job boards and social media platforms, and attending job fairs and industry events.

- Consider hiring remote workers

Even with all efforts in place, it may still be difficult to find the right talent in a business location. Today, technology has enabled people to work remotely. This offers access to a larger pool of candidates and also can help attract top talent from other parts of the country or even the world. It is also possible to work with freelancers or contractors to fill specific skills gaps on a project-by-project basis.

- Enhance the recruitment process

An inefficient recruitment process will cost the company good talent. Therefore, any poor communication or delayed communication will affect talent acquisition. A company might need to streamline its recruitment process.

Final Thoughts

The global tech talent shortage is already negatively affecting businesses. Since the shortage is expected to rise, business leaders need to decide on the best way forward so they are not left behind in digital transformation. A good decision should fit business goals whether choosing to hire internal talent, remote workers, or outsource technology needs.