Categories for

Increased Tax Bills Hitting Private Companies – Big and Small

Private companies both large and small are feeling the tax pinch due to changes in the law. With rampant inflation, labor shortages, lingering supply chain issues and increased borrowing costs due to rising interest rates, tax problems are the last thing struggling companies need to face.

While tax rates themselves remain largely unchanged, business’ taxable income is increasing due to changes in three main deduction areas: research and experimental (R&E) capitalization; interest expense deduction calculations; and a reduction in bonus depreciation. All of these provisions were made more liberal in the Tax Cuts and Jobs Act (TCJA) of 2018, but with a wind-down over a 10-year period.

Part of the problem is that these tax law changes can increase a business’ overall tax burden even though there have been no operational changes to the business, leaving less profits than prior years with all other factors being equal. Below, we look at each of the three tax provisions, the changes coming and the impact on businesses.

Stricter Interest Expense Limitations

Tax code section 163(j) limits the amount of business interest expense to 30 percent of adjusted taxable income. The 30 percent limit remains unchanged, but the basis of what constitutes “taxable income” as part of the calculation is becoming tighter.

From 2018 through 2021 year-end, businesses were allowed to add back depreciation, amortization and depletion in coming up with their adjusted taxable income that underlies the calculation. As a result, for 2022 and onward, without these add-backs the taxable income on which the 30 percent limit is applied will be lower, resulting in smaller interest deductions.

Given that borrowing rates have gone up substantially with increases by the Federal Reserve over recent years, now businesses are hit from two sides at once. They are likely to have higher interest costs but can take less as a deduction.

Research and Experimental Capitalization

At one point, business investments in research and experimentation under the TCJA were 100 percent deductible. Starting with 2022 and after, they need to be capitalized over a five-year period (15 years for foreign R&E).

Bonus Depreciation Decreases

Under the TCJA, bonus depreciation allowed immediate expensing and deduction of qualified investments in property and equipment, up through the taxable year-end of 2022. Starting with property and equipment investments placed in service in 2023, however, bonus depreciation is reduced from 100 percent down to 80 percent and decreases by an additional 20 percent each year until the taxable year 2027. From 2027 and onward, there will be zero bonus depreciations available. This will not only increase taxes, but it will also put a hamper on capital investments, rippling through the economy.

Conclusion

There is already chatter about extending some of these provisions, especially regarding bonus depreciation. Optimism on changes or extensions of these tax provisions should be taken cautiously, however. Many predicted that tax bill extenders would be in place before the end of 2022, but that never came to fruition. Right now, businesses are in a wait-and-see situation, with the threat of materially higher tax bills unless Congress does something.

New Employee Onboarding Best Practices: Factors to Consider for Success

According to one recent study, replacing an employee who has left your business can cost between 50% to 60% of that person’s salary. This is why it’s virtually always more expensive to hire a new person than it is to simply retain one of your existing workers. If you’re replacing someone who makes about $100,000 per year, it could cost between $50,000 and $60,000 just to get someone new in the door – and that’s before they’ve had a chance to start working.

If you need a single statistic that underlines the importance of employee onboarding, let it be that one.

Salaries are a huge part of the costs incurred when running a business, yes – but they’re also not the only expense of a high turnover. Not only does it delay the ability of your team to drive revenue, but it also significantly hurts employee morale in the long run.

Thankfully, you can take several steps during the employee onboarding process today that will help pave the way for success tomorrow.

The Age of Pre-Boarding is Upon Us

Truly, one of the most important things to understand about all of this is that it’s never too early to start preparing someone for their first day on the job. In recent years, many businesses have begun to engage in this prior to the start of the official “onboarding” process.

This is known as pre-boarding, and it can involve a number of things such as:

- Sending a new hire a welcome kit, which can include merchandise like t-shirts with company branding, a laptop or other assets that they’ll need once they get started, and more. If nothing else, you’ll know that they A) have access to certain tools, and B) you’ll have already begun making them feel like they belong.

- Sending “what to expect” messages. This is a great way to get someone’s expectations in order as early on in the process as possible. Let them know who they’ll be interacting with on their first day, for example, and what items they should bring with them.

- Conduct team introductions. For someone to be at their best, they need to feel like they’re contributing to the larger whole. To get to that point, you’ll want to introduce new hires to team members even before they begin onboarding in earnest.

Take Care of Administrative Tasks First

Once onboarding does begin, you’ll want to make sure that new hires have a “clear runway” to get to know the business and its culture, so to speak. This means completing all common onboarding tasks prior to someone’s arrival. If nothing else, this can help make sure that there are no unnecessary delays in their training and ongoing education.

Just a few of these tasks include but are not limited to things like:

- Making sure that all necessary security logins to your business’ technology, along with building access keys, have been accounted for.

- Setting up a new hire’s desk for them complete with necessary equipment like a computer, monitor, cables, adapters, and phone service. At the very least, you should make sure that they have a desk to report to in the first place.

- Create a profile for the new hire (complete with any associated logins) for any attendance tool that you’re using.

- If yours is the type of business that hands out uniforms and personalized name tags, these should be among the first things that the employee receives on their first day on the job.

Hit the Ground Running

New employees are always at their best when they’re engaged with your business. To get there, they have to be excited about their new job. This means that you should go out of your way to make this person’s first day, and the beginning of their larger onboarding experience, as exciting as possible.

If scheduling allows, arrange a lovely lunch with this new hire and a few of the people they’ll be working with. Send out an email to the entire business that introduces the new employee and lets people know when they’ll be starting and how exciting it is that they’ve arrived. You could even give them a gift for their first day.

In the end, it doesn’t matter how much experience a new hire has, or how impressive their resume is. They still need to be onboarded properly. Remember that if a chain is only as strong as its weakest link, your teams are only as strong as their weakest member. Don’t let that weak member be someone who wasn’t onboarded properly because, in that situation, the only people at fault will ultimately be company leadership.

Divorced, Separated, Married or Widowed this Year? Unpleasant Surprises May Await You at Tax Time

Taxpayers are frequently blindsided when their filing status changes because of a life event such as marriage, divorce, separation or the death of a spouse. These occasions can be stressful or ecstatic times, and the last thing most people will be thinking about are the tax ramifications. But the ramifications are real and need to be considered to avoid unpleasant surprises. The following are some of the major tax complications for each situation.

Separated – Separating from a spouse is probably the most complicated life event and is certainly stressful for the family involved. For taxes, a separated couple can file jointly, because they are still married, or file separately.

- Filing Status – If the couple has lived apart from each other for the last 6 months of the year, either or both of them can file as head of household (HH) provided that the spouse(s) claiming HH status paid over half the cost of maintaining a household for a dependent child, stepchild or foster child. A spouse not qualifying for HH status must file as a married person filing separately if the couple chooses not to file a joint return. The married filing separate status is subject to a host of restrictions to keep married couples from filing separately to take unintended advantage of the tax laws.

In most cases, a joint return results in less tax than two returns filed as married separate. However, when married taxpayers file joint returns, both spouses are responsible for the tax on that return (referred to as joint and several liability). What this means is that one spouse may be held liable for all of the tax due on a return, even if the other spouse earned all of the income on that return. This holds true even if the couple later divorces, so when deciding whether to file a joint return or separate returns, taxpayers who are separated and possibly on the path to a divorce should consider the risk of potential future tax liability on any joint returns they file.

- Children – Who claims the children can be a contentious issue between separated spouses. If they cannot agree, the one with custody for the greater part of the year is entitled to claim the child as a dependent along with all of the associated tax benefits. When determining who had custody for the greater part of the year, the IRS goes by the number of nights the child spent at each parent’s home and ignores the actual hours spent there in a day.

- Alimony – Alimony is the term for payments made by one spouse to the other spouse for the support of the latter spouse. Under tax law prior to tax reform, the recipient of the alimony includes it as income, and the payer deducts it as an above-the-line expense, on their respective separate returns. The tax reform rule is that alimony is non-taxable to the recipient if it is received from divorce agreements entered into after December 31, 2018, or pre-existing agreements that are modified after that date to treat alimony as non-taxable. Therefore, post-2018 agreement alimony cannot be treated by the recipient as earned income for purposes of an IRA contribution and can’t be deducted by the payer.

A payment for the support of children is not alimony. To be treated as alimony by separated spouses, the payments must be designated and required in a written separation agreement. Voluntary payments do not count as alimony.

- Community Property – Nine U.S. states – Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin – are community property states. Generally, community income must be split 50–50 between spouses according to their resident state’s community property law. This often complicates the allocation of income between spouses, and they generally cannot file based upon just their own income.

Divorced – Once a couple is legally divorced, tax issues become clearer because each former spouse will file based upon their own income and the terms of the divorce decree related to spousal support, custody of children and division of property.

- Filing Status – An individual’s marital status as of the last day of the year is used to determine the filing status for that year. So, if a couple is divorced during the year, they can no longer file together on a joint return for that year or future years. They must, unless remarried, either file as single or head of household (HH). To file as HH, an unmarried individual must have paid over half the cost of maintaining a household for a dependent child or dependent relative who also lived in the home for more than half the year (exception: a dependent parent need not live in their child’s home for the child to qualify for HH status). If both ex-spouses meet the requirements, then both can file as head of household.

- Children – Normally, the divorce agreement will specify which parent is the custodial parent. Tax law specifies that the custodial parent is the one entitled to claim the child’s dependency and associated tax benefits unless the custodial parent releases the dependency to the other parent in writing. The IRS provides Form 8332 for this purpose. The release can be made for one year or multiple years and can be revoked, with the revocation becoming effective in the tax year after the year the revocation is made.

Family courts often award joint custody to the parents. In that case, if the parents cannot agree on which of them will claim a child as a tax dependent, then the IRS’s tie-breaker rule will apply. This rule specifies that the one with custody the greater part of the year, measured by the number of nights spent in each parent’s home, is entitled to claim the child as a dependent. The parent claiming the dependency is also eligible to take advantage of other tax benefits, such as childcare and higher education tuition credits.

Alimony – See alimony under “separated”.

Recently Married – When a couple marries, their incomes and deductions are combined, and they must file as married individuals.

- Filing Status – If a couple is married on the last day of the year, they can either file a joint return combining their incomes, deductions and credits or file as married separate. Generally, filing jointly will provide the best overall tax outcome. But there may be extenuating circumstances requiring them to file as married separate. As mentioned earlier, married filing separate status is riddled with restrictions to keep married couples from taking undue advantage of the tax laws by filing separate returns. Best look before you leap.

- Combining Income – The tax laws include numerous provisions to restrict or limit tax benefits to higher-income taxpayers. The couple’s combined incomes may well be enough that they’ll encounter some of the higher income restrictions, with unpleasant tax results.

- Affordable Care Act – If one or both spouses acquired their health insurance through a government marketplace and were receiving a premium supplement, their combined incomes may exceed the eligibility level to qualify for the supplement, which may have to be repaid.

Widowed – When one spouse of a married couple passes away, a joint return is still allowed for the year of the spouse’s death. Furthermore, the widow or widower continues to use the joint tax rates for up to two additional years, provided the surviving spouse hasn’t remarried and has a dependent child living at home. This provides some relief for the survivor, who would otherwise be straddled with an unexpected tax increase while also facing the potential loss of some income, such as the deceased spouse’s pension and Social Security benefits.

If any of these situations are relevant to you or a family member, please call for additional details that may also apply with respect to your specific set of circumstances.

Tax Changes Coming After 2025

By now you have probably gotten used to the provisions in the Tax Cuts and Jobs Act (TCJA) that became effective January 1, 2018. But don’t forget, most of the tax changes made by the TCJA are not permanent and will expire (sunset) after 2025. This will have an impact on long range tax planning and will result in a mixed bag of tax increases and tax cuts. How it will impact individual taxpayers will depend upon which provisions of TCJA affect them. The following is a review of what will happen when TCJA expires if Congress doesn’t intervene.

Standard Deductions – The standard deduction is that amount of deductions you are allowed on your tax return without itemizing your deductions. The standard deduction is annually adjusted for inflation. In 2018, the TCJA just about doubled the standard deduction as illustrated in the table below that also illustrates the 2023 standard deduction amounts. With the expiration of TCJA the standard deduction will be cut roughly in half.

| HISTORICAL STANDARD DEDUCTIONS | |||

| Tax Year | 2017 (pre-TCJA) | 2018 (post-TCJA) | 2023 |

| Married Filing Joint and Surviving Spouse | $12,700 | $24,000 | $27,700 |

| Head of Household | $9,350 | $18,000 | $20,800 |

| Single | $6,350 | $12,000 | $13,850 |

| Married Filing Separate | $6,350 | $12,000 | $13,850 |

The increased standard deduction under TCJA benefited lower income taxpayers and retirees, whose itemized deductions often were just barely more than the pre-TCJA standard allowance. The increased standard deductions also meant fewer taxpayers claimed itemized deductions – roughly 10% of filers now itemize versus 30% before TCJA – which helped simplify these filers’ returns.

Personal & Dependent Exemptions – Prior to 2018, the tax law allowed a deduction for personal and dependent exemption allowances. One allowance was permitted for each filer and spouse and each dependent claimed on the federal return. For the year prior to the TCJA’s suspension of the exemption deduction, the exemption amount was $4,050, which would have been inflation adjusted to $4,700 in 2023. The deduction for exemptions phased out for higher income taxpayers.

Child Tax Credit – Prior to 2018 the child tax credit was $1,000 for each child below the age of 17 at the end of the year. With the advent of TCJA the child tax credit was doubled to $2,000 for each child below the age of 17 at the end of the year. This more than made up for the loss of a child’s personal exemption deduction for lower income families.

The child tax credit is subject to phaseout for higher income taxpayers. However, TCJA substantially increased the income phaseout thresholds as illustrated in the table below, so much so that the credit became available to middle-income taxpayers. Also of note is the fact that the phaseout thresholds for the credit are not inflation adjusted. As a result, each year the credit benefit is gradually diminished for higher-income taxpayers.

| CHILD TAX CREDIT INCOME PHASEOUT THRESHOLDS | ||

| Filing Status | Pre-TCJA | Post-TCJA |

| Married Filing Joint | $110,000 | $400,000 |

| Married Filing Separate | $55,000 | $200,000 |

| Head of Household | $112,500 | $200,000 |

| All Others | $75,000 | $200,000 |

If the credit is allowed to revert to the pre-TCJA amount of $1,000 and the lower income phaseout levels, it will have a significant negative impact on families.

You may recall that for one year during the Covid-19 pandemic, the child credit amount was increased to $3,000 or $3,600, depending on the child’s age, and other temporary changes were made. Some in Congress want to permanently bring back these enhancements, so that possibility could become part of any legislative negotiations surrounding the sunsetting or extension of TCJA provisions.

Home Mortgage Interest Limitations – Prior to the passage of TCJA taxpayers could deduct as an itemized deduction the interest on $1 Million ($500,000 for married taxpayers filing separate) of acquisition debt and the interest on $100,000 of equity debt secured by their first and second homes. With the passage of TCJA, the $1 Million limitation was reduced to $750,000 for loans made after 2017 and any deduction of equity debt interest was suspended (not allowed). A return to pre-TCJA levels will tend to benefit higher income taxpayers with more expensive homes and higher mortgages.

Tier 2 Miscellaneous Deductions – TCJA suspended the itemized deduction for miscellaneous deductions for tax preparation fees, unreimbursed employee business expenses, and investment expenses. Most notable of these is unreimbursed employee expenses which allowed employees to deduct the cost of such things as union dues, uniforms, profession-related education, tools and other expenses related to their employment and profession not paid for by their employer. Investment expenses included investment management fees charged by brokerage firms and tax preparation fees, including the cost of tax return preparation and tax planning expenses. These types of expenses were allowed only to the extent they totaled more than 2% of the taxpayer’s adjusted gross income.

Phaseout of Itemized Deductions – Prior to TCJA itemized deductions were phased out for higher income taxpayers. The phaseout thresholds were annually inflation adjusted and for 2017, the year prior to TCJA taking effect, the AGI thresholds were $313,800 for married taxpayers filing jointly (half that for married filing separate), $261,500 for single filers, and $287,650 for those filing as head of household. Under TCJA the phaseouts were suspended, which only benefited higher income taxpayers. If the phaseout is reinstated, it will negatively affect upper income taxpayers, and increase the complexity of their returns.

SALT Limits – SALT is the acronym for “state and local taxes”. TCJA limited the annual SALT itemized deduction to $10,000, which primarily impacted residents of states with high state income tax and real property tax rates, such as NY, NJ, and CA. Several states have developed somewhat complicated work-a-arounds to the $10,000 limits that benefit taxpayers who have partnership interests or are shareholders in S corporations. The elimination of the SALT limitation will favor those residing in states with a state income tax and those with larger property taxes.

Moving Deduction – Prior to the implementation of TCJA taxpayers were able to deduct unreimbursed job-related moving costs where there was an increased commuting distance of 50 miles or more from the prior home and provided the individual worked at the new location full time for 39 weeks of the first 52 weeks (39 weeks first year and 78 weeks in first 2 years for self-employed persons). The moving deduction for active-duty military members was not suspended by TCJA. A restoration of this deduction would benefit taxpayers who are relocating because of job change where the employer is not reimbursing the cost of the move.

Commuting Tax Benefits – Prior to TCJA, an employer could reimburse an employee up to $20 a month for commuting to work on a bicycle, the $20 ($240 annually) was not taxable to the employee, and the employer could deduct the $20. TCJA suspended that benefit for bike commuters for the years 2018 through 2025. In addition, although employers can provide a tax-free benefit to employees for transit passes, commuter transportation, and qualified parking, the employer is unable to deduct those expenses under TCJA. For 2023 the maximum monthly exclusion for these fringe benefits is $300 ($3,600 annually). The sunsetting of TCJA may provide an incentive for employers to once again provide bicycle commuting benefit to their employees.

Personal Casualty Losses – Personal casualty losses are part of the Schedule An itemized deductions. TCJA suspended these losses that did not result from a federally declared disaster. If this deduction is restored, individuals will be able to deduct unreimbursed losses that exceed $100 per casualty and to the extent that these casualties exceed 10% of the individual’s AGI for the year.

Estate Tax Exclusion – TCJA virtually doubled the inflation-adjusted estate and gift tax exclusion as illustrated in the table below. This benefited wealthier taxpayers with larger estates. Also illustrated in the table is the inflation adjusted amount for 2023.

| ESTATE AND GIFT TAX EXCLUSION | |||

| Tax Year | 2017 (pre-TCJA) | 2018 (post-TCJA) | 2023 |

| Maximum Exclusion | $5.49 Million | $11.18 Million | $12.92 Million |

Most taxpayers have estates well under the pre-TCJA exclusion amount and will not be affected by a restoration of the lower amounts. However, this is not true of wealthier taxpayers, especially considering the estate tax rate is currently 40%.

Tax Brackets – TCJA altered the tax brackets and although most taxpayers benefited, higher income taxpayers benefited the most with a 2.6% cut in the top tax rate. The table only reflects different tax brackets. They may or may not apply to the same levels of income.

| TAX BRACKETS | |||||||

| Pre-TCJA | 10% | 15% | 25% | 28% | 33% | 35% | 39.6% |

| Post-TCJA | 10% | 12% | 22% | 24% | 32% | 35% | 37%

|

A return to the pre-TCJA rates would have the largest negative effect on higher income taxpayers.

Alternative Minimum Tax (AMT) – As part of TCJA Congress did eliminate the Corporate AMT, and even though they had also vowed to eliminate the individual AMT, when the final TCJA was passed, it was still there. But they did include a modest increase of the AMT exemption amounts and a huge increase in exemption amount phase-out thresholds. These, in addition to several other regular tax changes made by TCJA that eliminated certain itemized deductions that caused the AMT in the past, virtually wiped away the AMT for most taxpayers that were affected by it in years before 2018. Depending what changes Congress makes when TCJA expires, the AMT could again cause grief for many taxpayers.

Qualified Business Income (QBI) Deduction – As part of TCJA, Congress changed the tax-rate structure for C corporations to a flat rate of 21% instead of the former graduated rates that topped out at 35%. Needing a way to equalize the rate reduction for all taxpayers with business income, Congress came up with a new deduction for businesses that are not organized as C corporations.

This resulted in a new and substantial tax benefit for most non-C corporation business owners in the form of a deduction that is generally equal to 20% of their qualified business income (QBI). If allowed to sunset with TCJA, businesses (generally small businesses) will lose a substantial deduction.

Of course, these potential changes assume Congress does not extend or alter them. And they aren’t the only tax issues impacted by the December 31, 2025, TCJA sunset date, but are probably those that will affect the most taxpayers. Depending upon your particular circumstances, these possible changes can potentially impact your long-term planning such as buying a home, retirement planning, estate planning, future tax liability and other issues. Please contact this office with any questions.

What’s Best, FSA or HSA?

Many employers offer health flexible spending accounts (FSAs) and health savings accounts (HSAs) as part of their employee benefits packages. Both plans allow you to set aside money to pay medical expenses with pre-tax dollars, providing a significant tax benefit. But which is the better option?

Although FSAs are only available through an employer, you may be able to open an HSA on your own if you have an HSA-eligible health plan through work, your spouse’s employer, private insurance, or the insurance marketplace.

How Health Flexible Spending Accounts Work – A Health Flexible Spending Account (FSA, also called a “flexible spending arrangement”) is a special account you put money into that you use to pay for certain out-of-pocket health care costs.

You don’t pay taxes on this money. This means you’ll save an amount equal to the taxes you would have paid on the money you set aside. Employers may make contributions to your FSA, but they aren’t required to. With an FSA, you submit a claim to the FSA (through your employer) with proof of the medical expense and a statement that it hasn’t been covered by your plan. Then, you’ll get reimbursed for your costs.

To learn more about FSAs, contact your employer for details about your company’s FSA, including how to sign up. Facts about Health Flexible Spending Accounts (FSA):

- The amount you can put into an FSA for 2023 is limited to $3,050 per employer. If you’re married, your spouse can put up to $3,050 in an FSA with their employer too. The amount is indexed for inflation each year.

You can use funds in your FSA to pay for certain medical and dental expenses for you, your spouse if you’re married, and your dependents.

o You can spend FSA funds to pay deductibles and copayments, but not for insurance premiums.

o You can spend FSA funds on prescription medications, as well as over-the-counter medicines with a doctor’s prescription. Reimbursements for insulin are allowed without a prescription.

o FSAs may also be used to cover costs of medical equipment like crutches, supplies such as bandages, and diagnostic devices like blood sugar test kits.

o You generally must use the money in an FSA within the plan year. But your employer may offer one of 2 options:

- It can provide a “grace period” of up to 2-½ extra months to use the money in your FSA.

§ It can allow you to carry over up to $610 per year (the 2023 inflation adjusted amount) to use in the following year.

Your employer doesn’t have to offer these options. If it does, it can be either one of these options, but not.

Don’t put more money in an FSA than you think you’ll spend within a year on things like copayments, coinsurance, drugs, and other allowed health care costs.

Health Savings Account (HSA) - Is a type of savings account that lets you set aside money on a pre-tax basis to pay for qualified medical expenses. By using untaxed dollars in a Health Savings Account (HSA) to pay for deductibles, copayments, coinsurance, and some other expenses, you may be able to lower your overall health care costs. HSA funds generally may not be used to pay premiums.

While you can use the funds in an HSA at any time to pay for qualified medical expenses, you may contribute to an HSA only if you have a High Deductible Health Plan (HDHP) — generally a health plan (including a Marketplace plan) that only covers preventive services before the deductible. For plan year 2022, the minimum deductible for an HDHP is $1,500 for an individual and $3,000 for a family. When you view plans in the Marketplace, you can see if they’re “HSA-eligible.”

For 2023, if you have an HDHP, you can contribute up to $3,850 for self-only coverage and up to $7,750 for family coverage into an HSA. HSA funds roll over year to year if you don’t spend them. An HSA may earn interest or other earnings, which are not taxable if used for qualified medical expenses. Some health insurance companies offer HSAs for their HDHPs. Check with your company. You can also open an HSA through some banks and other financial institutions.

Establishing and contributing to an HSA can be more than just a way for individuals to save taxes and gain control over their medical care expenditures. It can also be a retirement vehicle, especially for taxpayers who are maxed out on their other retirement plan options or who can’t contribute to an IRA because of the income limitations. There is no requirement that medical expenses must be paid or reimbursed from the HSA, so a taxpayer can maximize tax-free growth in the account by using funds from other sources to pay routine medical costs. Later, distributions can be used tax-free to pay post-retirement medical expenses. Or, if used for non-medical purposes, an individual aged 65 or older will pay income tax, but not a penalty, on the distribution. Unlike IRAs, no minimum distributions are required to be made from HSAs at any specific age.

| FSA and HSA COMPARISONS | ||

| DIFFERENCES | FSA | HSA |

| Funds not used for medical purposes carry over year to year | Limited | Yes |

| Contributions are pre-tax | Yes | Yes |

| Contributions may be tax deductible | — | Yes |

| You must have high deductible medical insurance to qualify | No | Yes |

| The plan is only available through an employer | Yes | No |

| Funds can be invested for tax-free growth | No | Yes |

| Can be used as a retirement vehicle | No | Yes |

| Plan belongs to employer | Yes | No |

As you can see, an HSA allows larger contributions and retirement options but requires high deductible medical insurance to qualify. While an FSA is only available if your employer offers an FSA as an employee benefit, but only has limited carryover of unused funds.

If you have further questions related to HSAs and FSAs, please give this office a call.

An Interview with Olivia Metz, RBF’s Tax Season Intern

Olivia joined the RBF team as an intern in January 2023, working both with the Audit & Assurance and Tax departments. Originally from Upper Moreland, PA, she is a senior at Millersville University studying Business Administration with a concentration in Finance and Management. After graduating in May 2023, Olivia hopes to gain additional work experience while pursuing and master’s degree and studying for her CPA license.

We talked to Olivia about what inspired her to pursue accounting, what a typical day as an intern looks like, and what drew her to working at RBF.

What inspired you to study accounting?

Two things. One: both of my parents work in the accounting and finance field, and they both really like their jobs.

Two: I’ve always been interested in making money and creating my own budget. When I was little, I would set up a stand on the corner of my street to sell bracelets with other girls in my neighborhood. I applied for my first job on my 14th birthday.

What does your role as an intern at RBF entail?

One of the best things about my internship is that I don’t do busy work or “intern” tasks. My work is the same work that everyone else at the firm does.

I started in the A&A department, putting together audit engagement letters and entering data from audit engagements the team was working on. I also got to observe the actual audit process.

When tax filing season started, I switched to working with the Tax department, preparing individual tax returns.

What does a typical workday look like for you?

On a typical day during tax season, I come into the office and start at my computer. I check my email and see what tax returns are in my work queue. Then I start working through those returns. If I need help or have questions, I visit someone’s office. That’s something I really like about my days in the office; everybody is willing to answer questions or walk through the steps with me and understand the next time I see it.

What are some of the most challenging things you deal with in your role?

The most challenging thing for me was learning the systems and software that the firm uses to prepare tax returns, a platform called UltraTax. I had never used software like this before so getting the hang of it was a challenge.

What is your favorite part of your internship?

The work environment – everybody here is friendly and easy to talk to. The environment feels very genuine, and everyone is very willing to help.

What drew you to RBF as a place to intern?

I was interested in working with RBF from the way they talked about the internship in the interview. They really conveyed that they wanted to teach me and expose me to a lot of things in the accounting field. During the interview, they mentioned doing auditing and tax, but also going out to see clients. The other places I interviewed made it seem like I would just be doing busy work.

I also really like that RBF is a smaller firm, so I have been able to meet everybody. There’s been more opportunity to build relationships than if I interned at a larger firm.

What advice would you give to students looking to intern with an accounting firm?

Take advantage of your school’s resources – use Handshake, for example.

And go into it with an open mind. Initially I was looking for a finance internship, and there was a lot of opportunity to learn and grow by taking an internship at RBF.

Want to Improve Your Cash Flow? Shorten the Amount of Time it Takes to Get Paid

To say that things are uncertain right now when it comes to the economy is, in all probability, a bit of an understatement.

Inflation is at levels we haven’t seen in decades. Employment costs are rising across the board. Materials in a number of industries are more expensive than ever – if you can even get them at all thanks to still-ongoing issues with the fragile global supply chain.

All of these issues can make it difficult for organizations to tackle one of their most essential challenges of all: cash flow. According to one recent study, approximately 82% of all businesses that fail do so due to poor cash flow management or just a general misunderstanding of the idea itself.

Thankfully, this is only a hurdle if you allow it to be. Modernizing your back office processes can, among other things, help to dramatically reduce the amount of time it takes to get paid. That in turn can help with any current or potential cash flow issues, which is an excellent position to be in.

Improving Cash Flow, One Change at a Time

By far, one of the best ways to reduce the amount of time it takes to get paid by clients and other vendors involves asking for payment deposits at the beginning of any new business relationship.

This particular method helps to accomplish a few different things all at once. For starters, if a client owes you $1,000 for a job that has already been completed, they’re more likely to settle the total balance if they’ve already paid $250 of it versus having paid none of it. If they’ve already put forth a deposit before any work even started, they’re motivated to quickly see things through to completion and are less likely to delay things any longer than they need to.

It’s also a great way to help get at least some money coming in the door all the time so if a client does end up paying the remaining balance late, you were able to get at least part of it ahead of time.

Another option that you’ll want to leverage has to do with switching to digital invoices. If you haven’t already done so, understand in no uncertain terms that this is no longer a recommendation – it is a requirement.

Think about it from a purely logistical perspective if nothing else. If you send an invoice to a client via USPS and it takes five business days to reach them, and then another five days pass before they act on it, and then another five days pass before you finally receive that payment check in the mail, that’s 15 full days (at an absolute minimum) where your money was in limbo. A digital invoice, on the other hand, can be sent in seconds and paid just as quickly. Not only that, but you’re freeing up the valuable time of your back-office employees so that they can focus on more important matters.

Not only that, but a lot of digital invoicing systems also integrate with a lot of the financial software that you’re likely already using. So you’ll have less paperwork to keep track of on your end and you’ll be able to easily see who has paid and who hasn’t (thus requiring a phone call to follow up). This will lead to more accurate financial statements overall, giving you a better foundation for making actionable decisions moving forward.

Finally, if you want to motivate people to pay you quickly, you need to give them as many options as possible when it comes to precisely that. The easier it is for someone to take your desired step, the more likely they are to take it.

Many businesses got away with just accepting cash or checks in the past but those days are no more. You should also, at a minimum, accept credit and debit cards. You could even choose to explore certain digital payment options like PayPal, Zelle, and others. Give people the chance to pay on their own terms and they’re less likely to delay the process any longer than necessary.

In the end, addressing cash flow concerns is not something that you “do once and forget about.” It’s an ongoing process that you must remain proactive about or else economic uncertainty (not to mention client or vendor uncertainty) could exacerbate things significantly. But by taking steps like asking for payment deposits, embracing digital invoices, and offering more options when it comes to paying, you can reduce the amount of time it takes to get paid at all – thus improving cash flow along the way.

When Can You Dump Old Tax Records?

Taxpayers often question how long records must be kept and the amount of time IRS has to audit a return after it is filed.

It all depends on the circumstances! In many cases, the federal statute of limitations can be used to help you determine how long to keep records. With certain exceptions, the statute for assessing additional tax is 3 years from the return due date or the date the return was filed, whichever is later. However, the statute of limitations for many states is one year longer than the federal limitation. The reason for this is that the IRS provides state taxing authorities with federal audit results. The extra time on the state statute gives states adequate time to assess tax based on any federal tax adjustments that also apply to the state return.

In addition to lengthened state statutes clouding the recordkeeping issue, the federal 3-year rule has several exceptions:

- The assessment period is extended to 6 years instead of 3 years if a taxpayer omits from gross income an amount that is more than 25 percent of the income reported on a tax return.

- The IRS can assess additional tax with no time limit if a taxpayer: (a) doesn’t file a return; (b) files a false or fraudulent return to evade tax; or (c) deliberately tries to evade tax in any other manner.

- The IRS gets an unlimited time to assess additional tax when a taxpayer files an unsigned return.

If no exception applies to you, for federal purposes, you can probably discard most of your tax records that are more than 3 years old; add a year or so to that if you live in a state with a longer statute.

Examples: Susan filed her 2020 tax return before the due date of April 15, 2021. She will be able to safely dispose of most of her records after April 15, 2024. On the other hand, Don filed his 2020 return on June 1, 2020. He needs to keep his records at least until June 1, 2024. In both cases, the taxpayers may opt to keep their records a year or two longer if their states have a statute of limitations longer than 3 years.

Important note: Even if you discard backup records, never throw away your file copy of any tax return (including W-2s). Often the return itself provides data that can be used in future tax return calculations or to prove amounts related to property.You should keep certain records for longer than 3 years. These records include:

- Stock acquisition data. If you own stock in a corporation, keep the purchase records for at least 4 years after the year you sell the stock. This data will be needed to prove the amount of profit (or loss) you had on the sale. Although brokers are now required in most cases to keep purchase records and report the information to the IRS when the stock is sold, it is still a good idea for you to maintain your own records, as you the taxpayer are ultimately responsible for proving the cost to the IRS if your return is audited.

- Stock and mutual fund statements where you reinvest dividends. Many taxpayers use the dividends they receive from a stock or mutual fund to buy more shares of the same stock or fund. The reinvested amounts add to basis in the property and reduce gain when it is finally sold. Keep statements at least 4 years after the final sale.

- Tangible property purchase and improvement records. Keep records of home, investment, rental property, or business property acquisitions AND related capital improvements for at least 4 years after the underlying property is sold.

As we become more and more a paperless society, you may wonder if you must keep the paper version of the records mentioned in this article. No, you don’t – the paper documents can be scanned and maintained on your computer or in the cloud. But if you do convert the records to electronic files, be sure to maintain a back-up that can be retrieved if you have a computer crash or cyber attack that takes over your computer.

If you have questions about what records to retain and what you can dispose of now, please give this office a call.

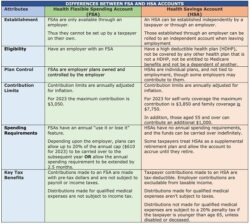

What is the Difference Between an HSA and a Health FSA?

The tax code provides two tax advantageous plans for taxpayers to pay medical expenses. One is a Flexible Spending Account (FSA) and the other is a Health Savings Account (HSA). The two are often misunderstood and their provisions are frequently mixed up by taxpayers who then fail to take advantage of the tax benefits available from these accounts.

This article explains the workings, qualifications, and tax benefits of each with a side-by-side comparison chart of the two programs. Both have a common theme: contribution to both is made withpre-tax dollars (they reduce taxable income) and distributions to pay qualified medical expenses are tax free.After that the two plans are quite different.

Flexible Spending Accounts (FSAs)

There are three types of FSAs: dependent care assistance, adoption assistance and medical care reimbursements. This article will only be dealing with the latter, often referred to as aHealth FSA.A Health Flexible Spending Account is part of a qualified cafeteria plan offered by an employer, that allows employees to contribute pre-tax dollars annually to be used by the employee to pay medical expenses of the employee, their spouse, and dependents during the year. The maximum contribution is annually inflation adjusted, and for 2023 is $3,050 (up from $2,850 in 2022).In the case of a married couple where each spouse has an FSA account with an employer, both can contribute the maximum.

Since an FSA is an employer plan, an employee cannot take it with them if they leave their employment. Thus, FSAs are not transferrable and cannot be rolled into an individual’s health savings plan.

Common Features of an FSA – Funds can be used for health insurance deductibles, copays, medication, and other health care related out-of-pocket costs. For ease of use, most FSA accounts come with a debit card. Employees can spend the money in the account before it’s fully funded.

FSA Allowable Medical Expenses Include Those For:

- The diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body,

- Prescription Drugs,

- Medication available without a prescription (an over-the-counter medicine or drug) that is prescribed),

- Insulin,

- Transportation primarily for and essential to medical care,

- Supplementary medical insurance for the aged,

- Feminine menstrual products, and

- Personal Protective Equipment (COVID)

No Double Dipping – Medical expenses reimbursed from the FSA cannot be claimed as a Schedule A medical itemized deduction.

Unused Amounts (Use It or Lose It) – Unused amounts at the plan’s year end are generally forfeited by the employee. However, a plan can have either:

- A grace period of up to 2½ months after the end of the plan year in which to use up the unused amount or

- Allow up to 20% of the annual contribution limit ($610 for 2023)of unused amounts from the end of the plan year to be used to pay or reimburse qualified medical expenses in the following year.

Unused amounts more than the carryover amounts are forfeited (cannot be returned to the employee). The carryover amount does not reduce the maximum contribution amount allowed for the carryover year.

FSA participants need to pay close attention to their FSA account balances to ensure they do not forfeit any funds at year’s end.

Health Saving Accounts (HSAs)

Individuals must meet the following requirements to contribute to an HSA:

- Not be claimed as a dependent on anyone else’s tax return.

- Not be enrolled in Medicare.

- Covered under a high-deductible health plan (HDHP) and not be coveredunder any other health plan which is not an HDHP, unless the other coverage is permitted insurance or coverage for accidents, disability, dental care, vision care, or long-term care.

Enrolled in Medicare – The IRS has interpreted being “enrolled in Medicare” to mean both eligibility for and enrollment in Medicare. An individual who is otherwise eligible, but who is not enrolled in Medicare Part A, may contribute to an HSA until the month enrolled in Medicare.

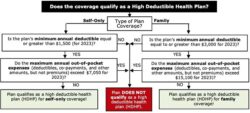

Covered Under a High-deductible Health Plan – HDHPs come in two varieties: Self-Only plans and Family plans. Use the flow chart below to determine if a plan qualifies as a high-deductible health plan.

HSA Contributions and Contribution Limits – Individuals may establish an HSA either independently or with their employer. If made with an employer, and the individual subsequently leaves the employment, the individual can roll the funds into their own HSA or take a taxable distribution subject to a 20% penalty.

In addition to the individual, others can make contributions to the HSA, including employers as well as other persons (e.g., family members) subject to the annual inflation adjusted contribution limits. Those limits for 2023 are:

- $3,850 for self-only coverage

- $7,750 for family coverage

- $1,000 additional amount for those aged 55 and older.

An account holder gets the deduction for contributions to his HSA even if someone else (e.g., a family member) makes the contributions. Employercontributions to an HSA are excluded from the employee’s income – so these contributions are not deducted on the employee’s tax return. Distributions for qualifying medical expenses are tax-free.

HSA Allowable Medical Expenses – Generally the eligible medical expenses are the same as allowed for FSAs. The qualified medical expenses must be incurred only after the HSA has been established. Medical expenses paid or reimbursed by HSA distributions cannot also be claimed as a medical expense for itemized deduction purposes.

HSA as a Supplemental Retirement Vehicle – Establishing and contributing to an HSA can be more than just a way for individuals to save taxes and gain control over their medical care expenditures. It can also be a retirement vehicle, especially for taxpayers who are maxed out on their other retirement plan options or who can’t contribute to an IRA because of the income limitations.

There is no requirement that medical expenses must be paid or reimbursed from the HSA, so a taxpayer can maximize tax-free growth in the account by using funds from other sources to pay routine medical costs. Later, distributions can be used tax-free to pay post-retirement medical expenses. Or, if used for non-medical purposes, a retiree aged 65 or older will pay income tax on the distribution, but not a penalty. Those younger than 65 who use their HSA funds for other than qualified medical purposes pay a penalty of 20% of the amount distributed in addition to income tax on the distribution. Unlike IRAs, no minimum distributions are required to be made from HSAs at any specific age.

FSA-HSA Comparison Table

The following table compares the key differences between Health Flexible Spending Accounts and Health Savings Accounts:

As you can see, either an FSA or HSA can help you pay your out-of-pocket medical expenses. On top of that, contributions are made on a pre-tax basis directly reducing your taxable income. If in an employer plan, in addition to reducing your taxable income, contributions reduce payroll taxes. Plus an HSA can be a supplemental retirement vehicle.

Please give this office a call if we can help you utilize the tax benefits of a health FSA or an HSA.

Don’t Get Hit with IRS Underpayment Penalties

Under federal law, taxpayers must pay taxes during the year as they earn or receive income, or they can find themselves falling victim to substantial underpayment penalties. Even worse, they may have spent the money, and when tax time comes are unable to pay their past taxes and spiral into financial distress.

To facilitate the pay-as-you-earn concept, the government has provided several means of assisting taxpayers in meeting that requirement. These include:

- Payroll withholding for employees – W-4;

- Pension withholding for retirees – W-4P;

- Voluntary withholding for Unemployment and Social Security benefits – W-4V; and

- Estimated tax payments for self-employed individuals and those with other sources of income not covered by withholding – Form 1040-ES.

Employees with primarily wage income can use the IRS online tool, the Tax Withholding Estimator, to determine if their withholding closely matches their projected tax liability or if they need to adjust their tax withholding by providing a revised Form W-4 to their employer.

Employees and those with significant income from other sources, multiple jobs, rentals, side gigs, children subject to the kiddie tax, capital gains, etc., may find it appropriate to consult with this office for a more sophisticated tax projection and estimate of needed withholding and/or estimated tax payments.

Individuals should also check their tax withholding and estimated payments when:

- Changes in tax law affect their situation.

- They experience a lifestyle or financial change like marriage, divorce, birth or adoption of a child, home purchase, retirement, or filed chapter 11 bankruptcy.

- They change jobs or have a change in wage income, such as when the taxpayer or their spouse starts or stops working or starts or stops a second job.

- They have taxable income not subject to withholding, such as interest, dividends, capital gains, self-employment and gig economy income, and IRA distributions.

- Reviewing their planned deductions or eligible tax credits, including items like medical expenses, taxes, interest expense, gifts to charity, dependent care expenses, education credit, Child Tax Credit or Earned Income Tax Credit.

- Nonresident alien taxpayers should determine their tax withholding using the special instructions in Notice 1392, Supplemental Form W-4 Instructions for Nonresident Aliens.

Once an individual has determined they need to change their tax withholding, the individual should complete a new Form W-4 to give to their employer. Individuals with other types of income should provide the payor with either a new Form W-4P or Form W-4V, as applicable. Those making estimated payments can mail the payment along with the Form 1040-ES to the address included on the form or use the IRS on-line payment system to make a payment electronically.

When a taxpayer fails to prepay a safe harbor (minimum) amount, they can be subject to the underpayment penalty. This nondeductible interest penalty is higher than what might be earned from a bank. The penalty is applied quarterly, so for example, making a fourth quarter estimated payment only reduces the fourth-quarter penalty. However, withholding is treated as paid ratably throughout the year, so increasing withholding at the end of the year can reduce the penalties for the earlier quarters. This can be accomplished with cooperative employers or by taking an unqualified distribution from a pension plan, which will be subject to 20% withholding, and then returning the gross amount of the distribution to the plan within the 60-day statutory rollover limit.

Federal law and most states have so-called safe harbor rules, meaning if you comply with the rules, you won’t be penalized. There are two Federal safe harbor amounts that apply when the payments are made evenly throughout the year.

- The first safe harbor is based on the tax owed in the current year. If your payments equal or exceed 90% of your current year’s tax liability, you can escape a penalty.

- The second safe harbor—and the one taxpayers rely on most often—is based on your tax in the immediately preceding tax year. If your current year’s payments equal or exceed 100% of the amount of your prior year’s tax, you can escape a penalty, regardless of the amount of tax you may owe when you file your current year’s return. If your prior year’s adjusted gross income was more than $150,000 ($75,000 if you file married separate status), then your payments for the current year must be 110% of the prior year’s tax to meet the safe harbor amount.

There is also a “de minimis amount due” of $1,000. If the amount owed is less than $1,000 the underpayment penalties do not apply.

Where taxpayers get into trouble is when their income goes up or their withholding goes down for the current year versus the prior year. Examples are having a substantial increase in income, such as when investments are cashed in, thereby increasing income but without any corresponding withholding or estimated payments. Another frequently encountered situation is when a taxpayer retires and their payroll income is replaced with pension and Social Security income without adequate withholding. Taxpayers who don’t recognize these types of situations often find themselves substantially underpaid and subject to the underpayment penalty when tax time comes around.

The bottom line is that 100% (or 110% for upper-income taxpayers) of your prior year’s total tax is the only true safe harbor because it is based on the prior year’s tax (a known amount), whereas the 90% of the current year’s tax amount is a variable based on the income for the current year, and often that amount isn’t determined until it is too late to adjust the prepayment amounts.

That being said, there are times when using the 100%/110% safe harbor method doesn’t make a lot of financial sense. For example, let’s say that in the prior year, you had a large one-time payment of income that boosted up your tax to $25,000, which is $10,000 more than you normally pay. You know that you won’t have that extra income in the current year. Rather than rely on the 100%/110% of prior tax safe harbor, where you’d be prepaying $10,000 more than your current year’s tax is likely to be, it may be appropriate to use the 90% of current-year tax safe harbor, determined by making a projection of your current year tax, and as the year goes along, monitoring your income and the tax paid in to be sure you are on track to reach the 90% goal.

Unlike employees, a self-employed individual must either estimate his or her net earnings for the year (or use the 100%/110% safe harbor) and pay taxes on a quarterly basis according to that estimate or safe harbor. Failure to do so will result in interest penalties.

Although these payments are called “quarterly” estimates, the periods they cover do not usually coincide with a calendar quarter.

| Quarter | Period Covered | Months | Due Date* |

| First | January through March | 3 | April 15 |

| Second | April and May | 2 | June 15 |

| Third | June through August | 3 | September 15 |

| Fourth | September through December | 4 | January 15 |

* If the due date falls on a Saturday, Sunday, or holiday, the payment is due on the next business day.

The rules discussed apply to federal pre-payments. The rules vary for the states.

Please contact this office for assistance. If you have a substantial increase in income, you should contact this office promptly so that your withholding or estimated tax payments can be adjusted to avoid a penalty.