Categories for Covid-19

CARES Act FAQ: Recovery Rebate

On March 27th, President Trump enacted the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The historic $2.2 trillion stimulus bill includes an estimated $300 billion in direct payments to eligible American taxpayers.

Below, we address some of the common questions regarding this particular initiative. If you cannot find the answer to your question, please do not hesitate to reach out to your Ross Buehler Falk & Company accounting advisor for further assistance.

Who is eligible for the recovery rebate?

To receive any portion of the recover rebate, you must fit all of the following three criteria:

- Be either a U.S. resident or citizen,

- Not be the dependent of another taxpayer, and

- Have a work-eligible Social Security Number.

Additionally, there is an income limit set for receiving the rebate:

- Single-filing taxpayers whose adjusted gross income (AGI) is under $75,000 are eligible to receive the whole amount; those whose AGI falls within $75,000 – $99,000 are eligible to receive a reduced rebate.

- For married filing jointly, those with AGI under $150,00 are eligible to receive the whole amount and those in the $150,000 – $198,000 range are eligible to receive a reduced amount.

- For those filing as head of household, the max AGI to be eligible to receive the full amount is $112,500 and the range for a partial rebate is $112,500 to $146,500.

How much is the recovery rebate?

The amount of your recovery rebate depends upon two factors: your adjusted gross income and how many children under the age of 17 you have. Taxpayers who qualify for the entire amount are eligible to receive $1,200 ($2,400 married filing jointly) plus $500 per child under 17. For the purposes of the recovery rebate, any child qualifies who is a qualifying child for the Child Tax Credit.

For taxpayers who earn above the $75,000/$150,000/$112,500 thresholds, the amount of the recovery rebate is reduced incrementally. For every $100 that the taxpayer’s AGI exceeds the phase-out threshold, their rebate is reduced by $5. In general, the point of total phase-out is $99,000 for single filers, $198,000 for married filing jointly, and $146,500 for heads of household. For taxpayers with children, the point of total payment phase-out shifts. For example, married couples with two children who have an AGI greater than $150,000 but less than $218,00 would receive a portion of the recovery rebate.

What do I have to do in order to receive the rebate for which I am eligible?

For most eligible recipients, no action needs to be taken. The IRS will use the information from taxpayers’ 2019 tax returns (if filed) or their 2018 return to determine eligibility.

How will I receive the payment?

For those who filed 2019 or 2018 tax returns online, the IRS will direct deposit the payment into the same banking account reflected in the return field.

What if the IRS doesn’t have my direct deposit information?

The Treasury Department is working to develop a web-based portal to allow individuals to provide banking information to the IRS. The back-up plan is for individuals to receive payments via checks in the mail.

What if I didn’t file a tax return for either 2018 or 2019?

The best way to ensure that you receive the recovery rebate, if you are eligible, is to go ahead and file a 2019 tax return. Additionally, you can watch the IRS website for further instruction. The CARES Act includes a mandate to the IRS to engage in a public campaign to alert taxpayers of their eligibility and offer instructions on how to receive the rebate if they have not filed tax returns for 2018 or 2019.

The CARES Act also instructs the IRS to use additional tools to locate and provide rebates to eligible individuals who normally do not file a tax return due to their low income (e.g., seniors whose only income is from Social Security and veterans whose only income is a veterans’ disability payment). The IRS can base a rebate on Form SSA-1099, Social Security Benefit Statement or Form RRB-1099. That said, individuals in this situation are encouraged to go ahead and file a 2019 return in order to receive their rebate more quickly.

Other individuals with little income and those on means-tested federal benefits (such as SSI) are also eligible for the rebate—even those with $0 of income. However, they must not be the dependent of another taxpayer and they must have a work-eligible social security number.

What if my 2019 income was above the threshold but I make significantly less in 2020?

The recovery rebate is structured as an advance on a tax credit that eligible taxpayers may claim on their 2020 tax return. As such, if your income in 2020 is lower than in 2019, you will earn any additional credit for which you are eligible when you file your 2020 tax return.

Will my rebate be reduced because I have past due debt (federal or state, including student loan payments) and/or owe back taxes?

No, those situations will not cause a reduction of your rebate. The CARES Act waives nearly all administrative offsets that would ordinarily reduce tax refunds. There is one administrative offset that will still be enforced—the offset for those who have past due child support payments that the states have reported to the Treasury Department.

Here are a couple scenarios to further illustrate how the recovery rebate works:

Scenario 1: Jane Doe, who files as an individual, had 2018 AGI of $63,500 (she has not yet filed her 2019 tax return so the IRS will look at her 2018 return). In this scenario, she is entitled to receive the full $1,200 check, regardless of her 2019 tax liability.

Scenario 2: John and Sally Smith, who file as a married couple with 2 children under the age of 17, had 2019 AGI of $125,000. In this scenario, they are entitled to receive a check for $3,400 as part of the individual stimulus payments.

CARES Act FAQ: Emergency Economic Injury Grants

On March 27th, President Trump enacted the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The historic $2.2 trillion stimulus bill includes $10 billion in funding to provide emergency grants to small businesses and nonprofits that apply for economic injury disaster loans.

Below, we address some of the common questions regarding this particular initiative. If you cannot find the answer to your question, please do not hesitate to reach out to your Ross Buehler Falk & Company accounting advisor for further assistance.

Who is eligible for an emergency economic injury grant?

Emergency economic injury grants are available to businesses and non-profits that apply for a Small Business Administration (SBA) economic injury disaster loan (EIDL). Typically, the timeline for EIDL approval and disbursement takes 3-4 weeks. That’s where the emergency economic injury grant comes in.

The goal of the emergency economic injury grant program is to provide a rapid funds advance within three days of the EIDL application. EIDL applicants simply need to request the emergency grant when they apply. The SBA will provide the grant within three days of receiving the EIDL application. Even if your application for the EIDL loan is denied, you do not have to repay the $10,000 emergency economic injury grant. That said, when you apply for the EIDL and request an emergency economic injury grant, you will be required to certify—under penalty of perjury—that you are eligible to receive an EIDL.

Please note: applicants must have been in operation on January 31, 2020 to receive the grant.

What can I use the emergency economic injury grant money for?

The grant can be used to provide paid sick leave to employees, maintain payroll, meet increased production costs due to supply chain disruptions, and/or pay business obligations (debts, rent, mortgage payments).

How do I apply for an emergency economic injury grant?

When you apply for an EIDL, you will have the opportunity to request the emergency grant at the same time. To apply for an EIDL, click here to visit the SBA website.

What if I apply for other SBA loan programs, like the Paycheck Protection Program?

You may apply for an EIDL, the emergency grant, and the Paycheck Protection Program (PPP). If you receive a loan through the PPP, the amount that is forgiven will be decreased by the $10,000 grant.

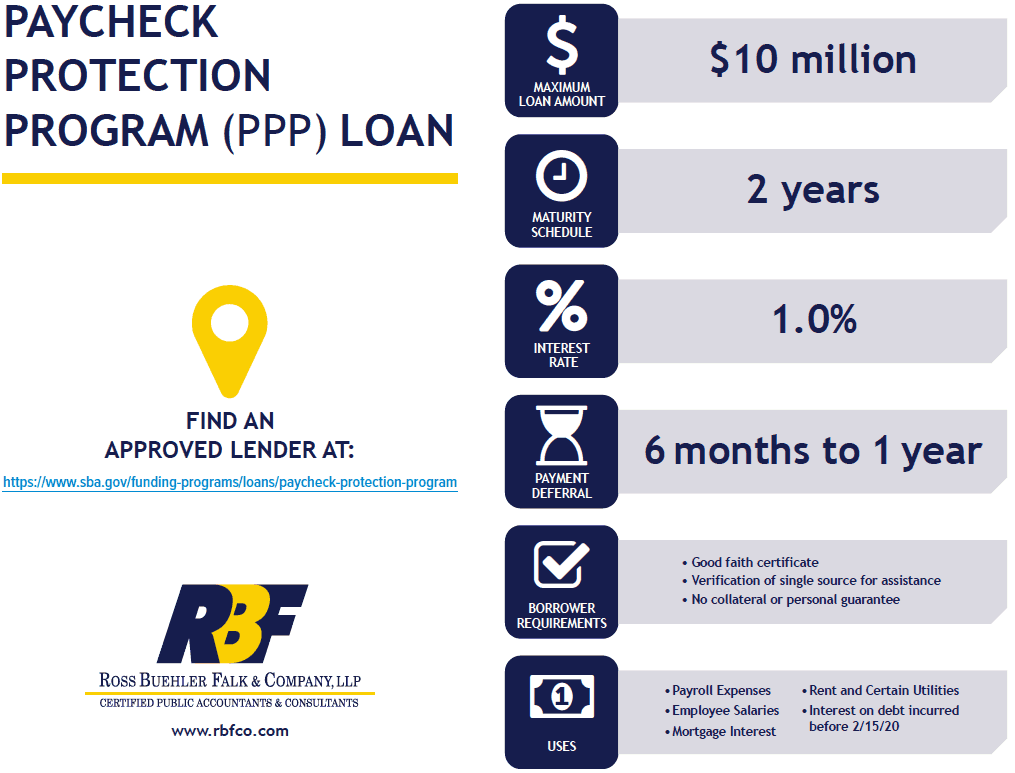

CARES Act FAQ: Paycheck Protection Program

On March 27th, President Trump enacted the Coronavirus Aid, Relief, and Economics Security (CARES) Act. The historic $2.2 trillion stimulus bill includes a $349 billion paycheck protection program (PPP) that targets aid to small businesses dealing with losses resulting from the coronavirus pandemic.

The PPP uses the already-existing small-business loan framework of the Small Business Administration (SBA) but includes some changes. The SBA was already impacted by provisions included in the March 6 stimulus law, the Coronavirus Preparedness and Response Supplemental Appropriations Act (CPRSA). The CPRSA expanded the qualification criteria for SBA loans under the organization’s Economic Injury Disaster Loan Program (EIDLP).

Below, we address some of the common questions we are encountering about the PPP. If you cannot find an answer to your question, please do not hesitate to reach out to your Ross Buehler Falk & Company accounting advisor for further assistance.

What is the Paycheck Protection Program?

The CARES Act designates $349 billion for general business loans to be distributed under section 7(a) of the Small Business Act during a designated “covered period,” February 15 through June 30, 2020. Borrowers can qualify for up to $10 million in 100% federal government guaranteed covered loans. Under the CARES act, the portion of these loans that is used for allowable purposes will be forgiven.

Who qualifies for the program?

Firstly, businesses and other entities seeking PPP loans must have been in operation on February 15, 2020. Eligible recipients include:

- Small businesses (fewer than 500 employees)

- Sole proprietors, independent contractors, and eligible self-employed individuals (see below for more details)

- IRC Section 501(c)(3) nonprofits

- IRC Section 501(c)(19) veterans’ organizations

- Tribal businesses under Section 31(b)(2)(C) of the Small Business Act (see below for more details)

For the purposes of the PPP, sole proprietors, independent contractors, and eligible self-employed individuals are those that are entitled to receive paid leave per the Emergency Paid Sick Leave Act. When applying, these individuals must submit documentation that establishes their eligibility (payroll tax filings, 1099s, and income/expense details for sole proprietorships). Tribal businesses that qualify are those with 500 or fewer employees (includes full-time, part-time, and other) or those that are the size standard established by the SBA for the industry in which they operate.

Eligible businesses can be precluded from receiving loans through the PPP by certain business affiliations. If the business is affiliated with a larger business (greater than 500 employees), they may be disqualified from participating in the PPP. An affiliation exists in two cases:

- One business controls another (or has the power to control it)

- A third party controls multiple businesses (or has the power to control them)

Additionally, the PPP expands eligibility to certain businesses with multiple locations, provided that each location has fewer than 500 employees. These eligible businesses have a North American Industry Classification System (NAICS) code that begins with 72 (accommodation and food services sector). The CARES Act waives affiliation rules for these businesses.

How much are the loans under the PPP?

The maximum loan amount is $10 million, though not every applicant is eligible for that much. There are three methods by which an entity’s loan amount can be calculated:

- For entities in business from February 15, 2019 – June 30, 2019: Calculate your average total monthly payments for payroll during the period and multiply it by 2.5.

- For entities that were not in business from February 15, 2019 – June 30, 2019: Calculate your average total monthly payments for payroll between January 1, 2020 and February 29, 2020 and multiply it by 2.5.

- For entities that took out an Economic Injury Disaster Loan (EIDL) between February 15, 2020 and June 30, 2020: You can refinance your loan into a PPP loan. Add the outstanding loan amount to the payroll sum.

How can the loan money be used?

Allowable uses of the PPP loans include:

- Salaries, wages, commissions, or similar compensations (up to $100,000 per year per employee, prorated)

- Cash tips or equivalent

- Employee leave, including parental, family, medical, or sick (excluding family or sick leave under the Families First coronavirus Response Act)

- Allowances for dismissal or separation

- Group healthcare benefits, including insurance premiums

- Retirement benefits

- State or local taxes on employee compensation (not including the employer’s share of FICA payroll taxes, railroad retirement act taxes, or other required U.S. income tax withholding)

- Continuation of group healthcare benefits during employee leave and insurance premiums

- Mortgage interest, rent, utility payments, and any other debt obligations incurred prior to February 15, 2020

Additionally, sole proprietors and independent contractors may use the loan money to cover compensation and income of up to $100,000 per year (prorated).

What if I use the money for a non-allowable purpose?

Loan money used for any of the allowable purposes listed above will be forgiven; loan money used for non-allowable purposes must be repaid. Any balance remaining after the amount used on allowable purposes is forgiven will continue to be a fully guaranteed loan for up to two years from the date of application.

What fees are associated with getting a PPP loan?

All service fees, prepayment fees, and borrower guarantees are waived for PPP loans.

What sort of collateral or personal guarantees are required?

Loans covered under the PPP require neither collateral nor personal guarantees, if the money is used for allowable purposes.

What is the interest rate on the loans?

The maximum interest rate is 1%.

Updated 4/3/2020 11:38 am.

What if I can obtain credit elsewhere?

While normally SBA loans only go to borrowers who cannot obtain credit elsewhere, for PPP loans, this requirement is waived.

How do I apply for the program?

The SBA and the Department of Treasury have approved thousands of institutions to be authorized lenders for the PPP. You can contact any local banking institution to find out if they are an approved lender, or use the Lender Match, an online tool from the SBA. Additionally, you can reach out to an SBA development center for local assistance in finding a lender.

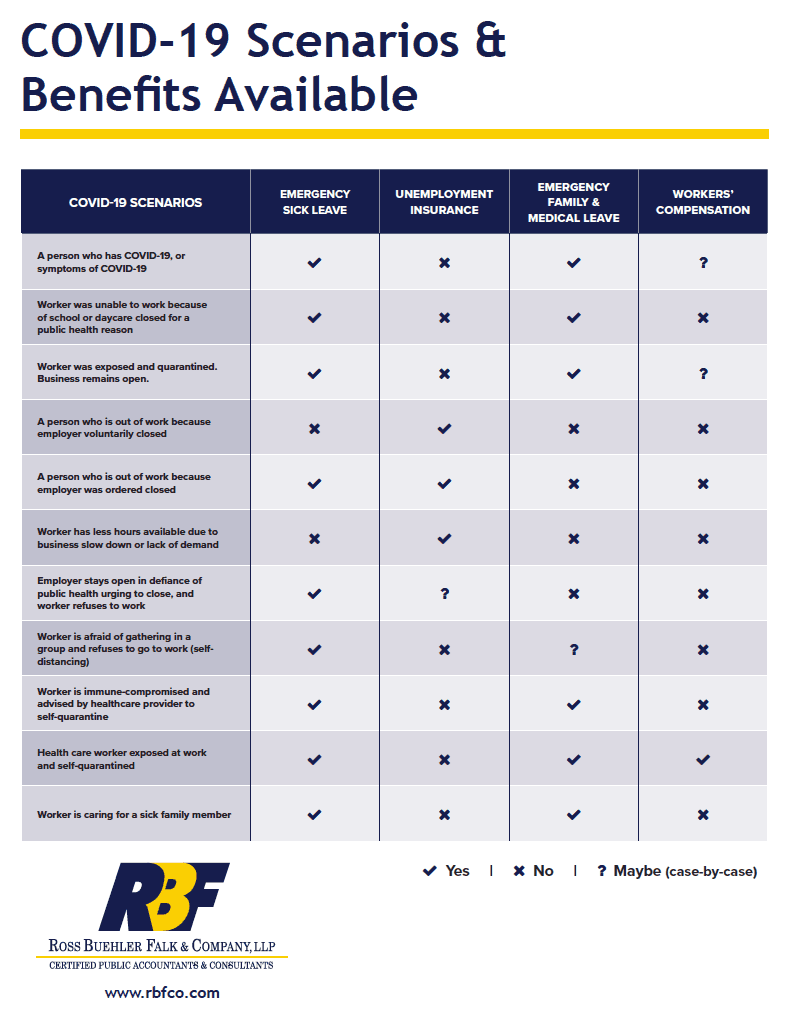

COVID-19 Scenarios and Benefits Available

The information on this flier is meant to give a general picture of benefits and rights available in certain COVID-19 work-related situations.

CARES Act Summary Coronavirus Relief: Phase Three

As of March 27, 2020, both the United States House and Senate have voted to pass a sweeping $2.2 trillion stimulus package designed to abate the economic damages caused by the coronavirus (COVID-19) pandemic. The Coronavirus Aid, Relief, and Economic Security (CARES) Act is the third piece of legislation crafted to address the economic havoc being created by COVID-19. The bill contains many provisions, including an expansion of unemployment insurance, direct payments to Americans, a loan guarantee program for industries, a suite of aid programs for small businesses, and more. President Trump has indicated that he will sign the bill into law. Details on the provisions included in the bill are laid out below.

Unemployment Insurance

Portion of the stimulus package: $260 billion (estimated)

The expansion of unemployment insurance, which Senator Chuck Schumer (D-NY) has referred to as “unemployment insurance on steroids,” is the greatest expansion of unemployment insurance benefits in decades. It expands the coverage window to four months, increases weekly benefits by $600, and extends coverage to the self-employed and gig workers. A secondary purpose of this provision is to allow companies to furlough workers, so they can stay on as employees and quickly return to work when the crisis is over. This portion of the bill is retroactive to January 27, 2020.

Individual Stimulus Checks

Portion of the stimulus package: $300 billion (estimated)

The Senate bill includes a provision for sending direct payments to Americans who earned less than $99,000 ($150,000 for couples without children) in adjusted gross income in 2019 (or 2018 if you haven’t yet filed your 2019 returns). Individuals who earned $75,000 or less will receive payments of $1,200 each; married couples who earned $150,000 or less will receive payments of $2,400. Those with children will receive an additional $500 per child. Beyond the $75,000/$150,000 threshold, the payment scales down and phases out entirely at $99,000/$198,000. Of course, if you have children, those payment scales shift slightly with the income limitation for adjusted gross income for a married couple with two children falling at $218,000.

Scenario 1: Jane Doe, who files as an individual, had 2018 AGI of $63,500 (she has not yet filed her 2019 tax return so the IRS will look at her 2018 return). In this scenario, she is entitled to receive the full $1,200 check, regardless of her 2019 tax liability.

Scenario 2: John and Sally Smith, who file as a married couple with 2 children under the age of 17, had 2019 AGI of $125,000. In this scenario, they are entitled to receive a check for $3,400 as part of the individual stimulus payments.

Keeping Workers Paid and Employed Act

Portion of the stimulus package: $350 billion+ (estimated)

The goal of this part of the bill is to prevent job loss and keep businesses from failing due to COVID-19. It provides $350 billion+ in “paycheck protection loans” to small businesses (defined as businesses with fewer than 500 employees and including sole proprietors and non-profits) to maintain their existing workforce and pay their obligations. These loans are fully guaranteed by the federal government through December 31, 2020. They will be limited to the average of monthly payroll costs over prior year multiplied by 2.5 AND any disaster loan that has been refinanced (capped at a total of $10M). A separate section of the CARES act allows for these “paycheck protection loans” to be forgiven on a tax-free basis. The amount to be forgiven is limited to an 8-week period beginning on the date of the loan and is a sum of the following expenses during that period:

- Payroll costs

- Mortgage interest

- Rent

- Certain utility payments

To receive forgiveness, the borrower would submit an application with documentation of expenditures. However, if the employer reduces their workforce or salaries (to employees that earn less than $100,0000), the forgiveness amount may be reduced.

Scenario 3: Avian Engineering had a total payroll of $1.8 million over the prior 12-month period (looking back from the date they apply for the loan under this portion of the Act). The monthly average payroll is $1.8 million/12 = $150,000 which is then multiplied by 2.5 to arrive at the total loan amount of $375,000, which is less than the $10 million cap. If Avian pays $300,000 in qualified expenses (detailed above) over the 8-weeks after the loan is granted, $300,000 of the $375,000 loan will be forgiven under the Act (so long as their workforce and salaries are not reduced during this time.

Business Tax Provisions

The CARES Act includes a wide variety of business tax provisions. In some cases, it enhances or modifies existing provisions; in other areas, it creates new tax provisions. Here is an overview of the business tax items included in the new legislation:

Net Operating Loss (NOL) – The CARES act modifies limitations on NOL that were implemented with the Tax Cuts and Jobs Act (TCJA). NOLs generated in 2018, 2019, or 2020 may now be carried back to the preceding five tax years. Additionally, the taxable income limitation has temporarily been removed, allowing NOLs to fully offset income.

Excess Business Loss – There is a provision for temporarily suspending the “excess business loss” limitation for non-corporate taxpayers. This allows these taxpayers to benefit from the NOL carryback modification.

Employee Retention Credit – This is a new credit created by the legislation. The credit is equal to 50% of up to $10,000 per employee in qualified wages, including qualified health plan expenses, for eligible employers. Eligible employers are those whose operations were fully or partially suspended OR those whose gross receipts declined by more than 50% (compared to the same quarter in 2019). The definition of qualified wages (QW) varies depending on if an eligible employer has greater than 100 full time employees or equal to or less than 100 full time employees.

- Greater than 100 full time employees: QW are wages paid to employees that are not providing services while the employer is considered an eligible employer.

- Equal to or less than 100 full time employees: QW are wages paid to all employees, whether or not they are providing services while the employer is considered an eligible employer.

Employer Payroll Taxes – The legislation allows for a deferral of the employer’s share of the Federal Social Security tax for both employers and self-employed individuals through December 31, 2020. The deferred amount must be paid over the course of the next two years. At minimum, half must be paid by December 31, 2021.

Business Interest Deduction – The 2017 TCJA limited business interest expense deductions to the sum of business interest income and 30% of adjusted taxable income. The CARES Act temporarily allows businesses to increase the amount of interest expense they deduct. To do so, it increases the limit of adjusted taxable income to 50% for 2019 and 2020.

Charitable Contribution Limits – For 2020, the limit on charitable contribution deductions is increased from 10% of taxable income to 25%. The limit on contributions of food inventory deductions is increased from 15% to 25%.

Qualified Improvement Property (QIP) – The CARES Act includes a key technical correction to an oversight in the TCJA. It reduces the depreciation window of QIP from 39 to 15 years and makes the change retroactive to January 1, 2018. This allows businesses to expense costs associated with interior improvements on nonresidential real property through bonus depreciation, rather than straight-line depreciation.

Federal Aviation Excise Tax – The legislation includes a temporary repeal of the Federal Aviation Excise tax. The repeal is effective from the date of enactment through December 31, 2020.

Alcohol Excise Tax Exception – For 2020, the Federal excise tax on distilled spirits is waived for spirits used to produce hand sanitizer.

Individual Tax Provisions

The CARES Act also provides a number of tax provisions for individuals, including:

Retirement Funds – Individuals may take distributions of up to $100,000 from qualified retirement accounts without incurring the 10% early withdrawal penalty. Within a three year window, the withdrawals can be recontributed regardless of the annual contribution cap. Additionally, tax on withdrawn income will be spread over three years. The funds may only be withdrawn for coronavirus-related purposes. To be eligible to withdraw, an individual must (1) be diagnosed with COVID-19, (2) have a spouse or dependent who is diagnosed with COVID-19, or (3) experience financial hardship as a result of COVID-19 (e.g., be quarantined, furloughed, laid off, etc.).

Required Minimum Distributions – For certain defined contribution plans and IRAs, the CARES Act offers a temporary waiver of the required minimum distribution rules for 2020.

Charitable Contributions – In order to encourage individuals to contribute to charitable organizations, the CARES Act includes a $300 deduction for contributions in 2020 for taxpayers who do not itemize their deductions. For taxpayers who do itemize deductions, the legislation includes an increase of the charitable contribution deduction.

Employer Payment of Student Loans – The legislation temporarily allows payments of qualified education loans to be included in the tax exclusion for employer-provided educational assistance. Employers may contribute up to $5,250 towards an employee’s student loans (and exclude the paid amount from the employee’s income). This is effective from the date of enactment through January 1, 2021.

Emergency Lending Fund for Industries

Portion of the stimulus package: $500 billion (estimated)

This portion of the bill makes federal loans available to large corporations, with some money earmarked for particular industries (e.g., $58 billion for airlines). In order to promote transparency and accountability, the following measures are imposed on corporations that receive loans through this program:

- Incentives to keep workers on the payroll

- Restrictions on executive compensation (with a two-year time-frame)

- Oversight from a Treasury Department Special Inspector General

- Oversight from an Accountability Committee

- Oversight from a Congressional Committee

- Ban on recipients performing stock buybacks for the length of the loan plus one year

- No organizations owned by Congressional leaders, President Trump, or his family, may receive loans through this program

- The names of recipients and terms of their loans will be public information

Emergency Aid to State, Local, and Tribal Governments

Portion of the stimulus package: $150 billion (estimated)

The package allocated $150 billion to be distributed among state and local governments, including county and tribal governments. Specifically, $8 billion is allocated to tribal governments.

Emergency Aid to the American Medical System

Portion of the stimulus package: $150 billion (estimated)

Described as “a Marshall Plan for the American medical system,” this portion of the Senate bill allocates $100 billion to bolstering the American healthcare system. The money will be made available to hospitals, nursing homes, Medicaid providers, community health centers, and other healthcare facilities. It can be used for a wide variety of purposes, including, but not limited to, personal protective equipment (PPE), testing supplies, additional Medicare funding, and COVID-19 research funding.

Support for the Department of Defense

Portion of the stimulus package: $10.5 billion (estimated)

Within the $10.5 billion, $1.4 billion is earmarked for any National Guard deployments and $1 billion is allocated to the Defense Production Act in order to support the creation of medical supplies.

Additional Items

The expansive legislation includes the following additional items:

- Support for childcare, education, senior housing, and more

- $25 billion (estimated) allocated to keep public transit systems afloat

- $25 million (estimated) for the John F. Kennedy Center for the Performing Arts

- $25 billion+ (estimated) to bolster food assistance programs, including food stamps

- $9.5 billion (estimated) to the Department of Agriculture to support agricultural producers

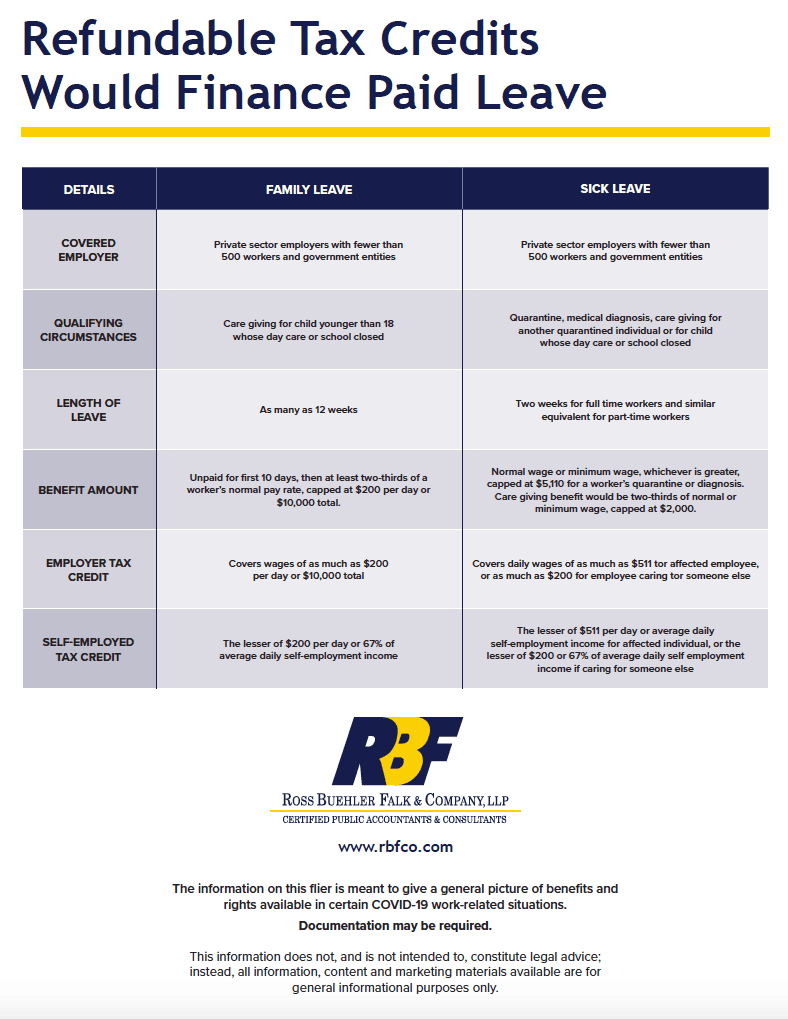

Do I Qualify for Paid Sick Leave Under the New Coronavirus Act?

On Wednesday, March 18, President Trump enacted a coronavirus emergency relief package, known as Families First Coronavirus Response Act. The legislation includes relief for American workers required to take time off work because of the coronavirus, the Emergency Paid Sick Leave Act of 2020.

The act includes both paid leave benefits for American workers and tax credits for American employers, to offset the financial burden. Additionally, self-employed taxpayers are eligible for the tax credit.

Paid Sick Leave Eligibility

The new legislation mandates paid leave for many American workers. Private employers with fewer than 500 workers and public employers are now required to provide paid sick leave to workers who are affected by the coronavirus. A worker must have been employed at the company for at least thirty days prior to being impacted by coronavirus to qualify.

To be eligible for paid sick leave under this act, a worker must meet one or more of the following criteria:

- They have been ordered to self-quarantine or isolate by a federal, state, or local authority.

- They have been warned to self-quarantine or isolate by a healthcare provider.

- They are currently seeking a medical diagnosis for coronavirus symptoms they are experiencing.

- They are caring for someone who qualifies under either criterion 1 or 2, above.

- They are caring for a child whose school, daycare, or other childcare provider is unavailable as a result of coronavirus concerns.

Additionally, to receive paid sick leave, an eligible worker must take 14 or more days of leave (due to one of the circumstances listed above) in a one-month period.

Paid Sick Leave Details

Full-time workers qualify for up to 80 hours (two weeks) of sick leave. Those who are sick or quarantined qualify for full pay, up to $511 per day (maxing out at $5,110). Those who are on leave to care for another person are eligible for two-thirds of their normal pay, up to $200 per day (maxing out at $2,000). Part-time employees are eligible for sick leave equal to the average number of hours they work in a two-week period.

Additionally, the new legislation enhances the Family and Medical Leave Act (FMLA) that governs employee absences in order to care for minor children. In the event that a worker’s child cannot go to school or daycare as a result of coronavirus closures, the worker qualifies to receive two-thirds of their regular salary, up to $200 per day (maxing out at $10,000). This aid only becomes available after the worker has already been on leave for 10 days.

Please note: these paid sick leave provisions are not permanent. This legislation expires on December 31, 2020.

Tax Credit Details

In order to help employers pay for the sick leave as outlined above, the legislation outlines a new payroll tax credit. Employers will be reimbursed for the full amount of sick leave coverage. The credit has the same limitations as the leave for workers: $511 per day for workers who take leave due to sickness or quarantine and $200 per day for workers who take leave to care for another person.

Self-employed taxpayers are also eligible for relief via these tax credits. The bill covers 100% of an equivalent amount of qualified sick leave for self-employed individuals who become ill or are quarantined. It covers two-thirds of an equivalent amount of qualified sick leave for self-employed individuals caring for a sick family member or a child whose school or daycare has been closed.

For full details, read the text of the Families First Coronavirus Response Act at congress.gov. Alternatively, click here for a detailed summary from the House Committee on Appropriations.

As always, please do not hesitate to reach out to your Ross Buehler Falk & Company accounting advisor with any questions or concerns. We are here to help.

What Does Paid Sick Leave Mean for My Organization?

On Wednesday, March 18, President Trump enacted a coronavirus emergency relief package, the Families First Coronavirus Response Act. The legislation includes relief for American workers required to take time off work because of the coronavirus, the Emergency Paid Leave Act of 2020. In order to help employers manage the cost of paid sick leave, the aid package also includes new tax credits designed to offset the financial burden.

The bill establishes payroll tax credits that are refundable through 2020 for employers with workers who take leave under the new paid leave programs (sick leave and/or family leave). The credit is equal to up to 10 days of leave wages per employee who goes on leave. For reference, here are the limits on sick leave and family leave included in the legislation:

- Sick leave guidelines:

- Eligible full-time workers who are sick or quarantined can receive wages equaling their full pay, up to $511/day (with a maximum of $5,110).

- Eligible full-time workers who are caring for an ill family member or child whose school or daycare has closed can receive wages equaling two-thirds of their regular pay, up to $200/day (with a maximum of $2,000).

- Eligible part-time workers can receive sick leave equal to the average number of hours they work in a two-week period.

- Family leave guidelines:

- Eligible workers who are caring for a child whose school or daycare has closed can receive two-thirds of their regular salary, up to $200/ day (with a maximum of $10,000)

The new tax credit comes in the form of a refund on an employer’s Social Security payroll tax. The credit has the same limitations as the leave for workers: $511 per day for workers who take leave due to sickness (maximum of $5,110) or quarantine and $200 per day for workers who take leave to care for another person (maximum of $2,000). Like the number of sick leave days, the tax credit is limited to 10 sick days per worker.

Additionally, the new legislation includes payroll tax credits for both the group health plan costs for workers on sick or family leave and the Medicare payroll tax on sick and family leave wages.

Employers who pay sick leave and family leave wages can expect to be reimbursed via a payroll tax credit for the entire amount. In the event that the tax credit exceeds what the employer owes in taxes, they will be given a refund for the remaining amount.

For full details, read the text of the Families First Coronavirus Response Act at congress.gov. Alternatively, click here for a detailed summary from the House Committee on Appropriations.

As always, please do not hesitate to reach out to your Ross Buehler Falk & Company accounting advisor with any questions or concerns. We are here to help.

8 Areas Where Small Businesses Should Anticipate Disruption

For more than six decades, the U.S. Small Business Administration (SBA) has been a resource for small business owners and entrepreneurs in the U.S. In response to the COVID-19 pandemic, the bureau created a resource page dedicated to helping small businesses learn to establish safe, secure, and healthy practices in the face of the outbreak.

The SBA enumerates areas in which small business owners should anticipate encountering difficulties during this time:

- Capital – Dealing with the COVID-19 outbreak will put a financial strain on small businesses. Shifting demand will have a big impact on revenue, inventory, and payroll. Business owners should strive to get out ahead by exploring various options for accessing capital.

- Workforce – The workforce will be impacted by both illness and business closures (both temporary and permanent). Workplace safety will be key for businesses that remain open.

- Inventory and Supply Chain – Rapidly changing demand will be difficult to meet. Suppliers’ inability to meet demand may impact your ability to keep inventory in stock.

- Cleanliness – In order to protect customers and employees alike, small businesses will need to implement new COVID-19 remediation and cleaning practices.

- Insurance Coverage – Businesses should review their insurance policies to determine coverage.

- Ability to Operate – It is possible that restrictions preventing some small businesses from operating will be imposed.

- Communication – Keeping open lines of communication with customers and clients is key during times of disaster.

- Preparedness – Small business owners should create contingency plans for dealing with the various possible scenarios.

For more details, visit the SBA website to view the list in full.

Charting New Territory: Business Strategy During the COVID-19 Outbreak

As the COVID-19 pandemic continues to unfold, business owners are facing a lot of uncertainty. It is not possible to know with confidence how events will continue to evolve over the next days, weeks, and months. However, there are some key steps that business owners can take to strive to mitigate damages and put themselves in the best possible position during this unprecedented time.

- Stay Home

Do your part to lessen the spread of COVID-19. This is nothing new, but it certainly bears repeating. As much as possible, limit contact with people outside of your home. If it is possible, work remotely, and have your employees do the same. Lead by example and encourage your team members to follow the COVID-19 protocols outlined by the Centers for Disease Control (CDC).

- Stay Informed

It might be tempting to shelter at home and check out of current events, but this is not a good strategy. Rather, you should try to review news on all levels—local, state, national, and world-wide. Compile a list of one or two reputable resources for each category and visit them online each day. Staying informed will help you as you consider what your strategy should be moving forward.

- Stay Alert

Focus your attention on developing strategies for maintaining the continuity of your business. Work with your teammates to develop plans for various contingencies that might play out over the next few weeks and months. Consider reaching out to your bank to establish or renew a line of credit to have available in the event that you might need it.

- Stay Focused on Your Clients

If your business can function with a remote team, then keep working! Be proactive about finding ways to go the extra mile for your clients. Put yourself in their shoes—what could you be doing for them that would be beneficial? How can you adjust your traditional practices to best meet the evolving needs of your customers and community?

- Stay in Contact with Your CPA

Now more than ever, you need good business advice. Do not hesitate to reach out to your accounting advisor in order to determine if they have any suggestions for you. We are partners in this together and our firm is committed to guiding you through these unprecedented times.

Resources for Small Businesses in Crisis

Many small businesses are reeling from the impact of the COVID-19 pandemic. Ross Buehler Falk & Company is here to help. We have gathered a list of helpful resources for small businesses to turn to during this unprecedented time.

Federal Health Resources

The President’s Coronavirus Guidelines for America – A short PDF with information about how each person can do their part to lessen the spread of COVID-19.

The Centers for Disease Control and Prevention (CDC) webpage on COVID-19 – This page is regularly updated and offers a wealth of helpful guides and information, including:

- Interim Guidance for Businesses and Employers – Strategies for employers to use now, future planning considerations, tips for creating an Infectious Disease Outbreak Response Plan, and additional links to resources.

- Environmental Cleaning and Disinfection Recommendations – Detailed guidelines for cleaning and disinfecting facilities with either suspected or confirmed COVID-19 contamination.

- Traveler’s Health Notices – The latest guidelines for travel.

Federal Business Resources

Guidance on Preparing Workplaces for COVID-19 – An in-depth document from the Occupational Safety and Health Administration (OSHA) offering insights on how COVID-19 will likely impact workplaces, directions for reducing workplace exposure risk, and more.

Small Business Guidance & Loan Resources – Assembled by the U.S. Small Business Administration (SBA), this webpage offers a wide variety of helpful information, including:

- The Economic Injury Disaster Loan Program – The SBA works with small businesses and non-profits that have been severely impacted by disasters, including the COVID-19 outbreak. The program provides low interest working capital loans.

- Search for SBA Local Partners – Discover local assistance initiatives and resource partners near you.

- SBA Contracting Guide – Information on aid and assistance for small businesses with federal contracts.

State Health Resources

State Business Resources

Ross Buehler Falk & Company is Here to Help

Do you have any additional questions? Would you like help finding local resources? Please don’t hesitate to reach out to Ross Buehler Falk & Company today.